U.S. Policy Implications of Global Peak Oil Demand

Back in the beginning of the century James Kuntsler published the book The Long Emergency which warned about societal collapse due to declining oil production combined with “climate change, resurgent diseases, water scarcity, global economic instability and warfare to cause major trouble for future generations.” Twenty years ago it was a pretty plausible argument as it was clear we were running out of new oil discoveries, there were no new technologies on the horizon to replace oil, and climate change appeared to be a thing.

In a plot twist, it appears the world is currently producing more oil than it needs. Unfortunately all of the other things Kuntsler predicted are now happening. However, two things have happened in those twenty years that weren’t expected in 2005. The first was the success of fracking for oil and gas in America. The world would have very likely hit a point where we needed more oil then we could produce but fracking unleashed a new type of oil production and business model which ultimately led to oil having a negative price in 2020. The world was producing more oil than it could use or store and thus, if you were an oil producer in America, you couldn’t give it away. Of course fracked oil and gas is more expensive to produce and also worse for the climate and environment so this development had its obvious downsides for humanity.

The second plot twist was the rapid advancements in renewable energy production and storage technologies combined with the cost for these technologies falling by well over 90% percent in those two decades. There is certainly no doubt that the world is facing a climate emergency due to the continued production and burning of fossil fuels, but it looks different from the one Kuntsler predicted in 2005. As we face the current long emergency of unfolding climate disaster, this new energy landscape likely requires some new thinking. It appears we are rapidly approaching a point of peak oil demand. This has a lot of interesting implications I believe we need to understand as we attempt to navigate this energy transition and address the climate emergency.

Peak oil demand will be good news for the climate — but not great news. Emissions are still increasing. Dangerous levels of warming are already baked in. And we are talking about the oil industry. This is an industry that lies about everything and is run by people willing to trade the future of the world for huge personal profits. Last month an Energy Transfer gas pipeline exploded in Houston. The week before we learned from the WSJ that the CEO of Energy Transfer has “a $46.5-million ranch in Colorado, a castle-like home in Dallas, and a private island in Honduras, where visitors can ride a zip line over a lagoon and nearby sharks.” These people don’t care about anything but money. And peak oil consumption will mean less money for them. So we could be facing a dangerous industry that realizes the real money making days are behind it. If you think they were bad before – they could get much worse.

A Bad Bet?

Oil markets are fickle when it comes to pricing. Small movements in supply and demand can cause really big movements in price. Oil prices are low right now. On an inflation adjusted basis, oil is at its lowest price in 20 years. Has global oil demand peaked? No. It’s just growing more slowly than expected. So we have a global market with increasing demand and falling prices. This is what a decrease in the rate of demand growth can do if there is slightly more supply than demand. And the money people are starting to pay attention. Last month for the first time in history, more people were betting the price of oil would go down than go up.

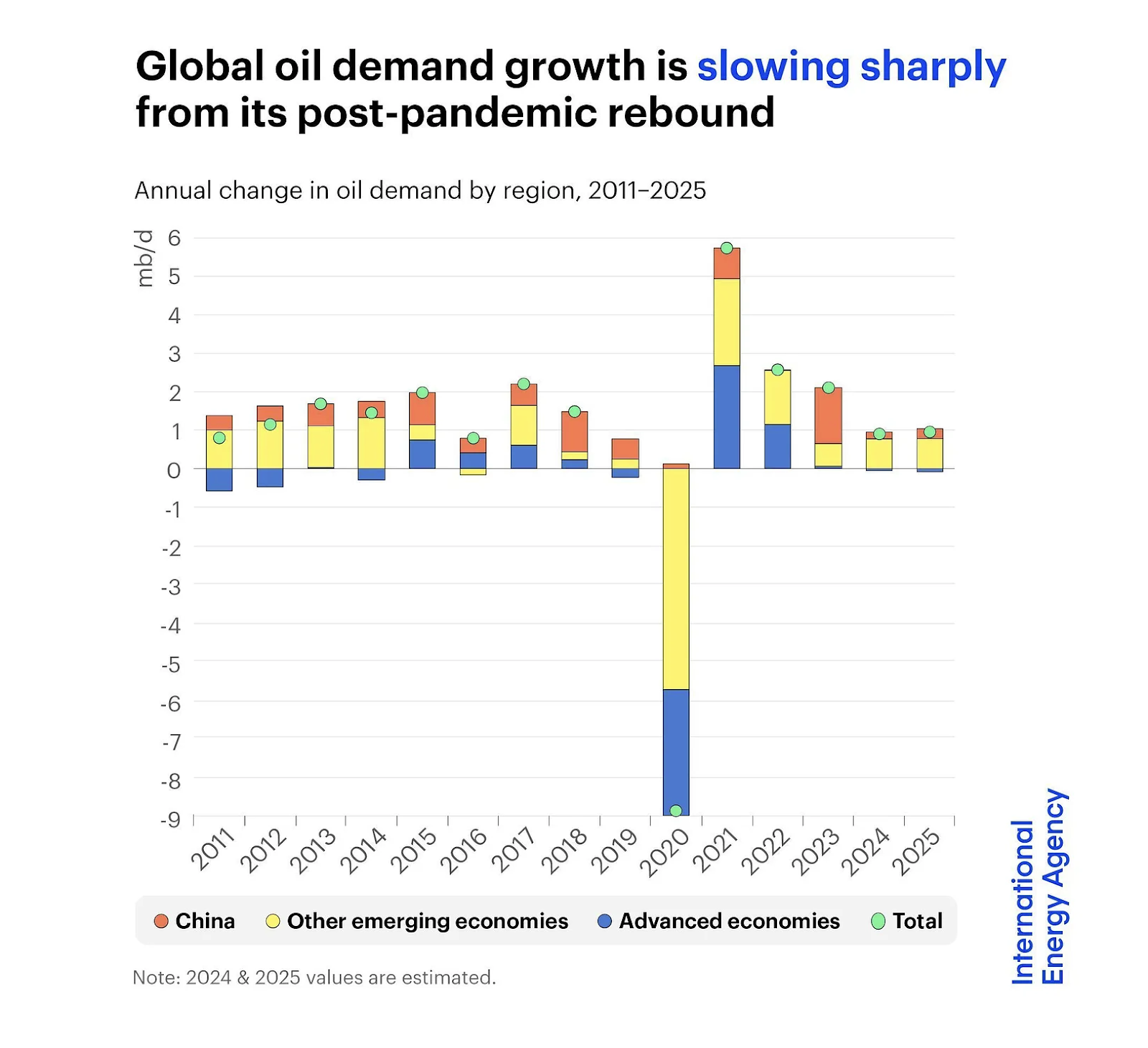

The global oil market is unique in many ways including that the major players regularly meet to talk about price fixing and market manipulation in a group called OPEC. However, in reality OPEC is run by the Kingdom of Saudi Arabia. And the Saudis are working hard to keep oil prices higher by intentionally keeping a lot of oil in the ground. Historically this has been a great way to increase oil prices. But something has changed and that change is global oil demand growth. OPEC has been trying to tell the world that oil demand growth is strong and will continue to be strong for decades but reality tells a different story.

Source: IEA

Structural Changes in Global Oil Market

I recently wrote about Exxon’s prediction that electric vehicles would not impact global oil demand. I’m still not sure why anyone would invest in a company that is saying such idiotic things other than that many do not see the structural changes happening in the oil markets. A year ago I wrote this:

It wasn’t a widely held opinion at the time but more people are coming around to this conclusion. Last month in the well-titled Wall Street Journal article, “The High-Stakes Spat Over How Much Oil the World Really Needs” they noted the likelihood of structural changes.

Stimulus from China’s central bank announced on Tuesday might help, but the recent slump looks structural as well as cyclical. In July, sales of electric vehicles and hybrids overtook those of internal-combustion engines there for the first time, and industrial trucks in the country increasingly run on liquefied natural gas rather than diesel.

I’ve been reading Gregor MacDonald’s newsletter ColdEye for the past few years. MacDonald has been right about the oil markets and demand for quite a while. I recommend paying attention to him on this topic. In his September newsletter he points out the changes in global oil demand, the current low price of oil, the very poor returns for oil investing and notes one other important change.

“It’s long been said that keeping a portion of one’s portfolio exposed to commodities can be a good way to keep up with inflation. But oil has entirely failed in this regard, having fallen behind most asset classes like stocks, real estate, precious metals, art, and collectibles.”

Something has clearly changed. Which leads MacDonald to ask an important question:

“That’s how we should think of the oil business: who in their right mind would want to get involved with it?”

China’s lower economic growth is likely the new normal

I’m often critical of the inability of the mainstream financial press to accurately report on the U.S. oil and gas industry. However, their ability to report on China’s economy is far worse. For the past year there have been comments in numerous articles noting that the reason global oil consumption is lower than expected is that China’s economy has slowed down. Here is a recent headline from CNBC.

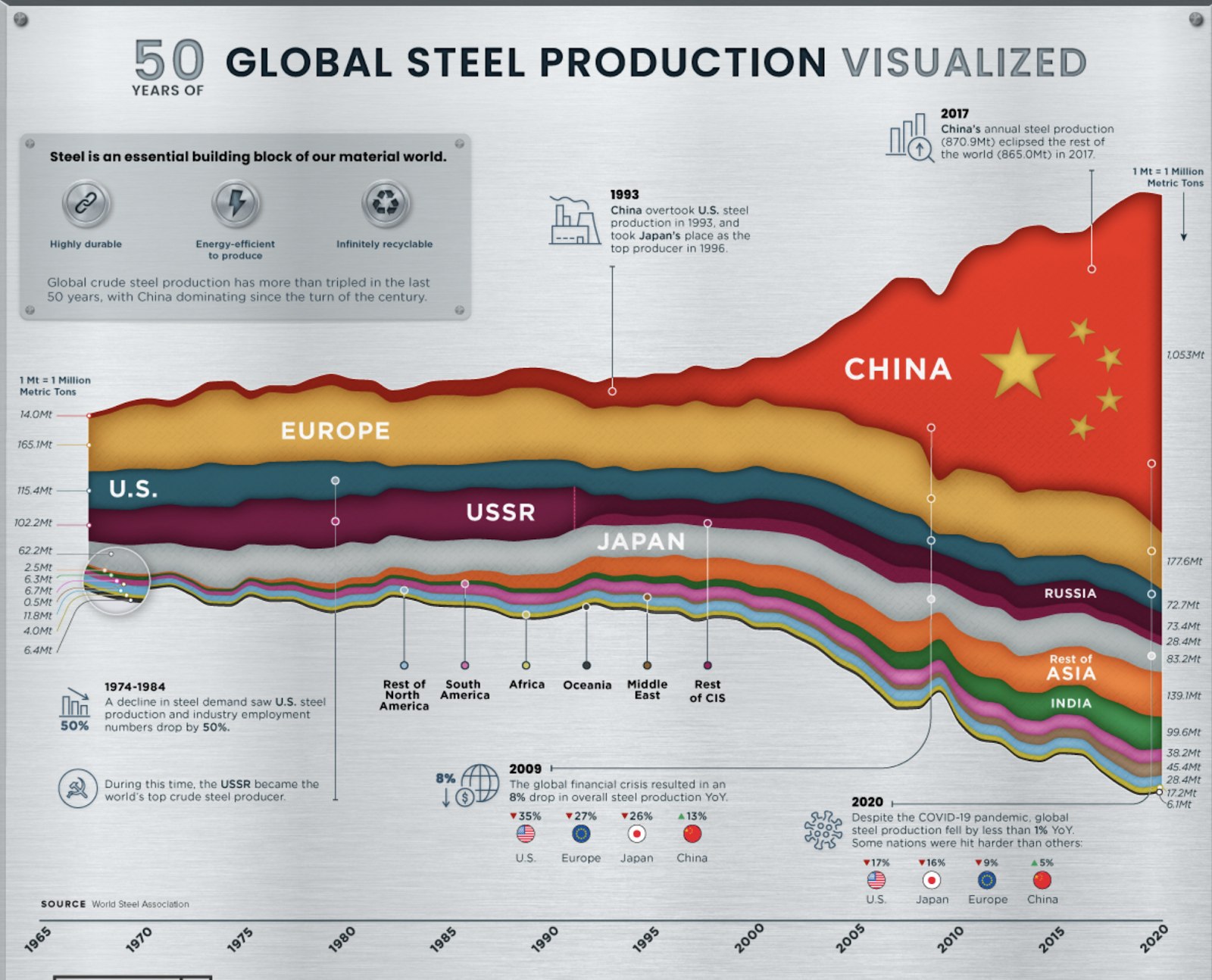

This is a convenient argument if you want to push the narrative of robust future global oil consumption that Exxon and OPEC are pushing. But is it true? China’s economy is definitely not growing at the pace it did for the past two decades. However, the insane growth of that period would be impossible to maintain. Take a look at this visualization of how China took over the global steel market in the first two decades of this century.

Source: Visual Capitalist

That sort of growth happened across the economy. And it simply can’t continue. Now China’s GDP is growing at around 5% a year. Significantly higher than the rate of growth in the U.S. economy. Next year China might only grow at 4%. Meanwhile, China’s population is declining. Which is another reason why it’s highly unlikely China will return to the double digit growth rates it saw at the peak of growth in the past 20 years.

The idea that it is China’s “sputtering” economy that is causing the global slowdown in oil consumption will not age well. China’s economy is changing along with the rest of the world and the transition away from oil has begun.

Also, while we are told China’s economy is sputtering and the U.S. economy is strong, China has taken over the global electric vehicle market. And the global battery market. And the global solar market. And the global electrolyzer market for making green hydrogen.

If this is how China dominates the world even while its economy is supposedly sputtering, what would happen if it returns to much stronger growth?

Either way, the reason that China is using less oil is that it is moving to technologies that don’t require oil and its economy is growing at lower rates, which is to be expected in an industrialized economy with declining population.

What Does This Mean

It is clear that the rise of alternative energy solutions — from solar power to electric vehicles — is having an impact on global oil consumption. And this change is likely to accelerate. Lower consumption means lower prices and now it appears that the Saudis are tired of keeping their oil off the market to try to keep prices higher. Last week they warned they plan to begin pumping more oil which could send global oil prices to $50 a barrel.

Will continued and expanding war in the Middle East change this? Quite possible, in the short-term. But as we saw with the impact of the fossil fuel-based war in Ukraine, these conflicts are now convincing many countries to speed up their transition to clean energy to reduce their dependence on imported oil and natural gas and the volatile pricing that comes with it.

However, the reality is that the U.S. oil industry is a money-loser at $50 a barrel. That price will reveal the industry-pushed fraudulent claims that they can make money at low prices. Will the transition to clean energy result in consistently low oil prices in the future? Highly likely. Which means U.S. oil companies will be making far less money which guarantees two outcomes we all need to care about:

1) The industry will not address methane emissions if it costs them any money.

2) The industry will continue to walk away from its massive environmental liabilities.

It is likely the U.S. oil industry will be asking for a bailout in the future. Bailing out failing industries is a bad deal for the public. The better idea is a buy-out. In July Kate Aronoff published a paper about public ownership of the oil and gas industry. I believe this will be the only realistic option. California’s oil industry is already financially underwater. At $50 oil, most of America’s oil industry is financially underwater and that is before their unfunded cleanup liabilities are factored in.

It will not surprise me if major investors in U.S. oil companies will be pushing for public ownership in a decade. They will be happy to unload the dying industry with huge debts. We should be planning for that now.

The U.S. oil industry made big money with the high oil prices after the Ukraine invasion. And yet at the same time the U.S. government is giving billions of dollars to clean up old oil industry wells and contamination and yet, as this article states, “Billions of dollars to clean up abandoned oil and gas wells will only make a dent.”

If we can’t get them to pay what they owe us when they are making record profits, it’s foolish to think they would do so when losing money.

If they lied about everything from climate science to their methane emissions when they were making money, why would we trust them to address the issue when they are not?

California’s oil market already has liabilities greater than its assets. That future awaits the American oil industry as a whole. At $50 oil, it will happen much sooner.

It’s clear that if we want the money, we need to get it now. Public ownership of the industry is likely the only way that happens. We will not address the climate crisis without a managed phase out of fossil fuel consumption. Leaving that up to the oil CEOs, the commodities traders and private equity groups that are buying up oil and gas assets is a recipe for climate failure.

Comments ()