U.S. Oil Industry Peaks as “the days of easy oil are over”

In October, shortly after Exxon and Chevron announced over $100 billion in combined acquisitions, oilfield services company Halliburton’s CEO Jeff Miller warned about the reality of producing oil in the U.S. shale industry.

“The reality is you have to do more work in order to stay flat.” This is an acknowledgement of the dreaded Red Queen effect for shale oil production. This is the situation where you have to do more just to keep production flat (aka running faster just to stay in place) because fracked shale oil wells decline much faster than conventional oil wells. This isn’t a new concept. Reuters reported on it in 2013 saying, “Shale production has been likened to Lewis Carroll's Red Queen Race, in which more and more new wells will need to be drilled just to offset rapidly declining output from existing holes.”

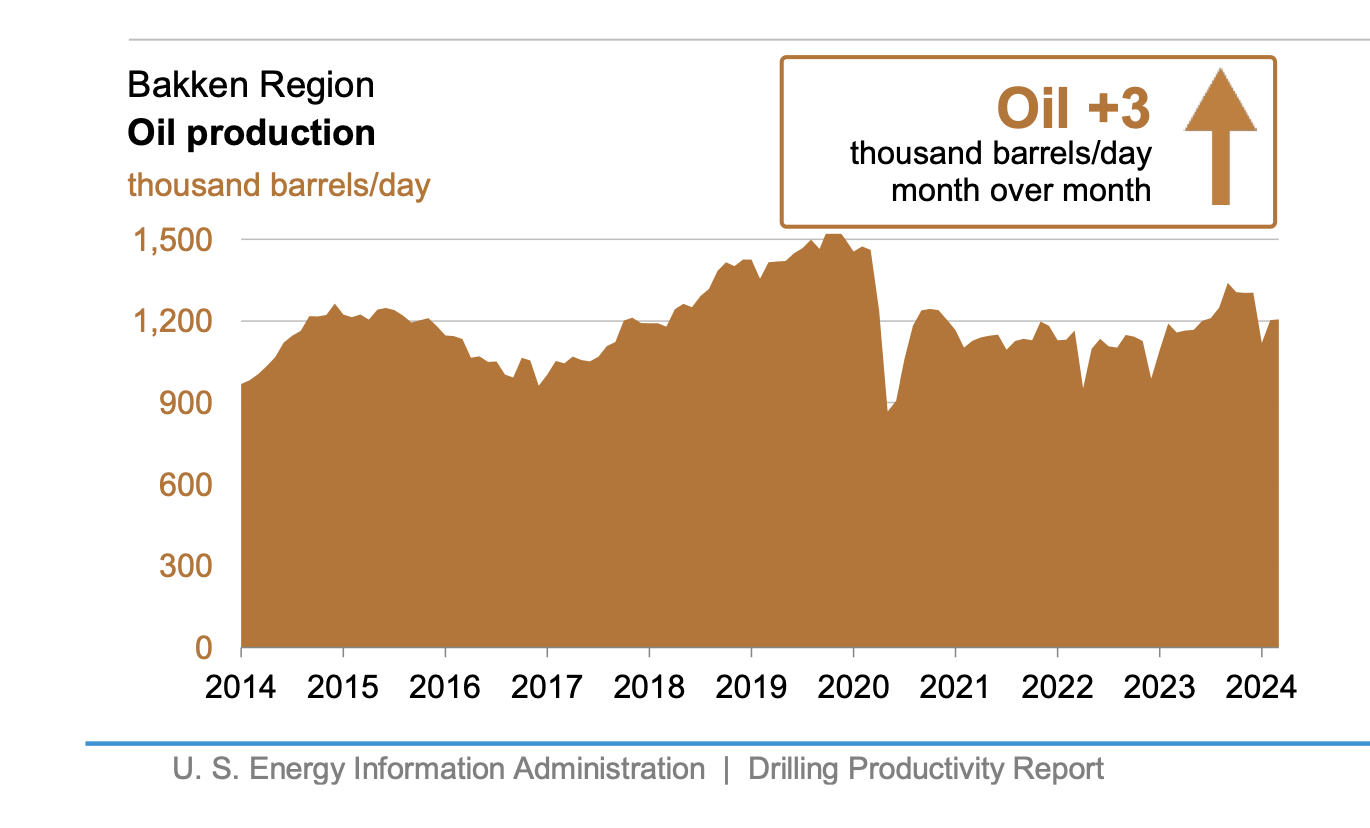

So as time passes, you have to keep doing more to just maintain production, while trying to do that when the acreage you have left to drill is less productive. This can be easily seen in the Bakken shale play in North Dakota. In December 2023 the Bakken had a record number of producing wells. And production fell. And it is well below the peak Bakken volume from 2020. That is the Red Queen at work. Just like in the Eagle Ford. And, very soon, the Permian.

Source: EIA

The title of the article that quoted Jeff Miller also explained the situation happening in the U.S. oil industry, “Exxon and Chevron Megadeals Reveal Why Days of Easy Oil Are Over.”

With all of the positive spin about these megadeals in the U.S. oil industry, the truth is these deals were necessary to change the story and distract from the reality of the impending oil declines facing the U.S. shale industry. The days of easy oil are over and yet, for most of those days for the past decade, the U.S. shale oil industry lost money. The reality is it will now get harder to make money in the U.S. shale oil industry. There is plenty of oil left in the shale plays of America, it’s just going to cost significantly more to extract than can be justified with $80 a barrel oil. All the while, the industry must drill more wells just to maintain production.

I began to write about the impending peak in Permian oil production in 2020. In that article I wrote, “The lack of remaining tier one acreage is something that even Exxon and Chevron can’t change.” While the recent massive acquisitions by those two companies give them more acreage, most of it isn’t tier one. And now, many are saying the peak for U.S. oil production is here as tier one acreage runs out.

Growing Agreement on Peak Shale

While Pioneer Resources former CEO Scott Sheffield recently predicted that U.S. oil production could grow to 15 million barrels per day from the current 13 million barrels per day, he wasn’t reflecting the growing consensus that the Permian is peaking. But then again, he will get paid a $29 million bonus if Exxon buys his company, so he is in a unique position to hugely benefit in the very near term if everyone thinks that the future for U.S. oil production is bright.

Meanwhile, there is growing consensus that the Permian is peaking, something that has been evident for the past few years to those paying attention.

Enervus is a leading provider of oil industry data for those interested in understanding what is truly happening based on actual data. In September 2023, Hart Energy ran an article titled, “Analysts: Top-Tier Drilling Inventory Shrinking as Well Costs Rise” which quotes Enervus managing director Dane Gregoris saying, “We’ve just sort of reached a point of maturity in U.S. shale. Wells aren’t getting better incrementally. In fact, they’re probably getting worse.”

Wells getting worse is one thing. But costs rising is another big one that the oil industry is trying hard to mislead the public about by claiming they have new technology to address this. They don’t.

In January, Bill Weatherburn, a commodities economist at Capital Economics summed up the situation with the U.S. oil industry saying, "we expect U.S. crude production to peak in 2024 and then decline gradually thereafter.”

In January longtime oil industry analyst Art Berman wrote a piece titled, “Beginning of the End for the Permian.”

Even the ever optimistic U.S. Energy Information Administration now says they expect U.S. oil production to decrease in the first half of 2024, before reaching a new record in 2025.

This piece by HFI Research is more optimistic than most and predicts U.S. oil peaking in 2025 after some growth in 2024.

If you don’t read Mike Shellman’s OilyStuff site, I recommend you start. This piece on the economics of shale oil production is highly informative and makes it much easier to understand why “the days of easy oil are over.” OilyStuff is also the home to some recent posts by user Anne which are enlightening as well. Anne writes, “Still betting that at some point in the next few months we'll be reading about the Big Surprise - that US oil tight oil production seems to have peaked in 2023.” Anne makes this comment while reporting on the latest oil production numbers reported by the EIA which showed total U.S. oil production declined in December, 2023 — as did Texas oil production.

The Implications of U.S. Oil In Decline

While we can only speculate on the motivations of the oil CEOs making these acquisitions in a shale industry that is peaked or peaking, it certainly will buy them a few years of not having to explain why they aren’t producing more oil as promised, which means a few more years to greatly increase their personal wealth with executive compensation. Exxon is still facing a lawsuit over its promise to produce 1 million barrels per day in the Permian by 2024. While the Pioneer purchase doesn’t negate the validity of that lawsuit, it does give them a reset on their production numbers and now they will be producing 1.3 million barrels per day in the Permian thanks to their $60 billion purchase.

Exxon and others want us to believe that technology will unlock more profitable oil from the Permian but, as I explained, this is highly unlikely. They want us to believe they can breakeven at $30 a barrel oil when the number is a likely double that (reread this if you doubt that). They want you to believe that there is big upside to U.S. oil production. But there isn’t.

We need to start facing the reality of where the U.S. oil industry is at and what that means. As I wrote last month, it is highly likely Exxon overpaid for Pioneer resources. Why would they do that? It only makes sense if they plan to walk away from the cleanup bill.

The big players in the U.S. oil industry just doubled down on shale oil. They are doing their best to mislead everyone about how much it costs to produce the oil. They are doing their best to mislead everyone about how much oil is in the ground. And they are fighting efforts by states, like Colorado and California to hold them accountable for the cleanup costs for the mess they have made.The industry had peaked. What isn’t clear is how fast it will decline if the industry can’t keep pace with the Red Queen. The only plan that makes sense for these companies investing vast sums in the remaining shale acreage in America is to take the profits that are left and use them for stock buybacks and dividends. That is the part where they privatize profits. And then they will hand the bill to the American public for the cleanup once the profit taking opportunities are gone. That is the part where they socialize losses. It’s already happening. It’s what the coal industry has done. If the U.S. public wants the oil and gas industry to pay to clean up its mess, it better get the money now, because just like production from a fracked shale oil well, the opportunity to get that money is rapidly declining.

This is the fifth article in a series detailing the current trends in the U.S. oil industry. The series will continue discussing the reality of the industry and will conclude with recommendations on policies to protect the American public and the global climate from the U.S. oil industry.

Comments ()