The U.S. Shale Oil Industry Asks You to Believe in Technology as Savior…Again

This article is the fourth in a series about the current state of the U.S. oil industry and how the industry is setting itself up to take the remaining profits it can and then stick the U.S. public with the cleanup bill.

If you listen to them, the current confidence of U.S. oil industry leaders is not based on the performance of current oil operations or on its oil reserves but instead on the promise of new “technology.” In June, Exxon CEO Darren Woods made this case to try to explain how Exxon would get to one million barrels per day of production in the Permian (something he originally said would happen this year, which led to fraud accusations and a lawsuit because it didn't happen).

"My challenge to the organization was to double recoveries and to find technologies that could unlock that," Woods said. "There is still a lot of oil being left on the ground."

Exxon’s elusive one million barrels per day Permian production goal is now a thing of the past after its $60 billion acquisition of Pioneer Resources. While the two company’s current combined production output is 1.3 million barrels per day, Woods has now predicted that Exxon will produce 2 million barrels per day by 2027. How could such a boost in production be possible in a peaking Permian which is quickly running out of high producing well inventory? We are told that “technology” will do this.

"When combined with our technology and industry-leading operational capabilities, we know that together, we can unlock far more value than either of us could alone," Woods said on a conference call discussing the Pioneer acquisition. Woods makes it pretty clear that the success of this deal requires technological advances that have yet to be achieved. However, there is a big difference in challenging your staff to “double recoveries” and actually doubling recoveries.

This seems pretty clear. What doesn’t seem as obvious is that because the industry just spent around $125 billion on shale oil acreage that will require new technology to make it a good investment, that this in itself guarantees said technology will actually be developed. And even if it is, will it be profitable? One lesson we should have learned from the fracking industry is that just because your technology can do something previously not possible (e.g. frack for shale oil), doesn’t mean you can make money doing it.

However, we are also being presented with the odd logical argument that, of course the technology exists, because it would be unthinkable to justify these massive expenditures without having that locked down.

Alex Beeker, research director at Wood Mackenzie explained to the Financial Times that “...all these deals have validated that there’s still a lot of efficiency improvements to go.” If you believe that, I suggest you read through my series on the systemic fraud involved in the U.S. shale industry. Last week’s Wall Street Journal article that went so far as to put the words “American oil” and “peak” in the same headline, had a more realistic take on the promise of technology.

“The ease in growth has gone, unless somebody comes up with a very dramatic new technical innovation,” said Paul Horsnell, head of commodities research at Standard Chartered Bank.

It’s pretty clear that U.S. shale oil growth is gone…unless someone comes up with “a very dramatic new technical innovation.” Why might this outcome be highly unlikely? Because we’ve heard it all before.

History Rhymes in the Permian

In 2019, I wrote a piece titled, “Fracking 2.0 Was a Financial Disaster, Will Fracking 3.0 Be Different?” which included this opening:

Two years ago, the U.S. fracking industry was trying to recover from the crash in the price of oil. Shale companies were promoting the idea that fracking was viable even at low oil prices (despite losing money when oil prices were high). At the time, no one was making money fracking with the business-as-usual approach, but then the Wall Street Journal published a story claiming all of this was about to change because the industry had a trump card — and that was technology.

Would it surprise you to learn that Exxon's efforts in the Permian was the focus of that article, too? And that they were promising that artificial intelligence could find out how to profit from shale oil. In addition to AI, we were also told that the industry has two new technological solutions to make shale oil profitable. Longer wells and cube development.

At the time, gas producer EQT was drilling new record wells that were four miles long which was both a technical record and a financial disaster. The WSJ later reported on that effort saying, “The decision to drill some of the longest horizontal wells ever in shale rocks turned into a costly misstep costing hundreds of millions of dollars.” The other technological solution touted was the new approach of cube development. Encana, the company highlighted back then that tried cube development ended up sending a letter to its employees stating, “The company intends to gradually separate employees between now and May 31, 2019.” Meanwhile, the U.S. shale oil and gas industry continued to gradually (and sometimes suddenly) separate investors from their money with promises it will be different this time.

Exxon’s New Promising Technologies

Investors have fallen for the promises of the U.S. shale oil industry many times before. Promises of magic fracking sand, huge production increases and of “world-class assets” that didn’t produce profitable oil have resulted in lawsuits alleging fraud from burned investors who believed what they were told by the industry. Now Exxon is asking investors to believe that they are the leaders in the new technologies that will make the Permian prolific and profitable. According to an article by Hart Energy that was published after the announcement of Exxon’s acquisition, those technologies are — longer wells up to four miles long and cube development.

That is the plan. These are not “very dramatic new technical innovations” but technologies that have been tried before and failed to produce profits.

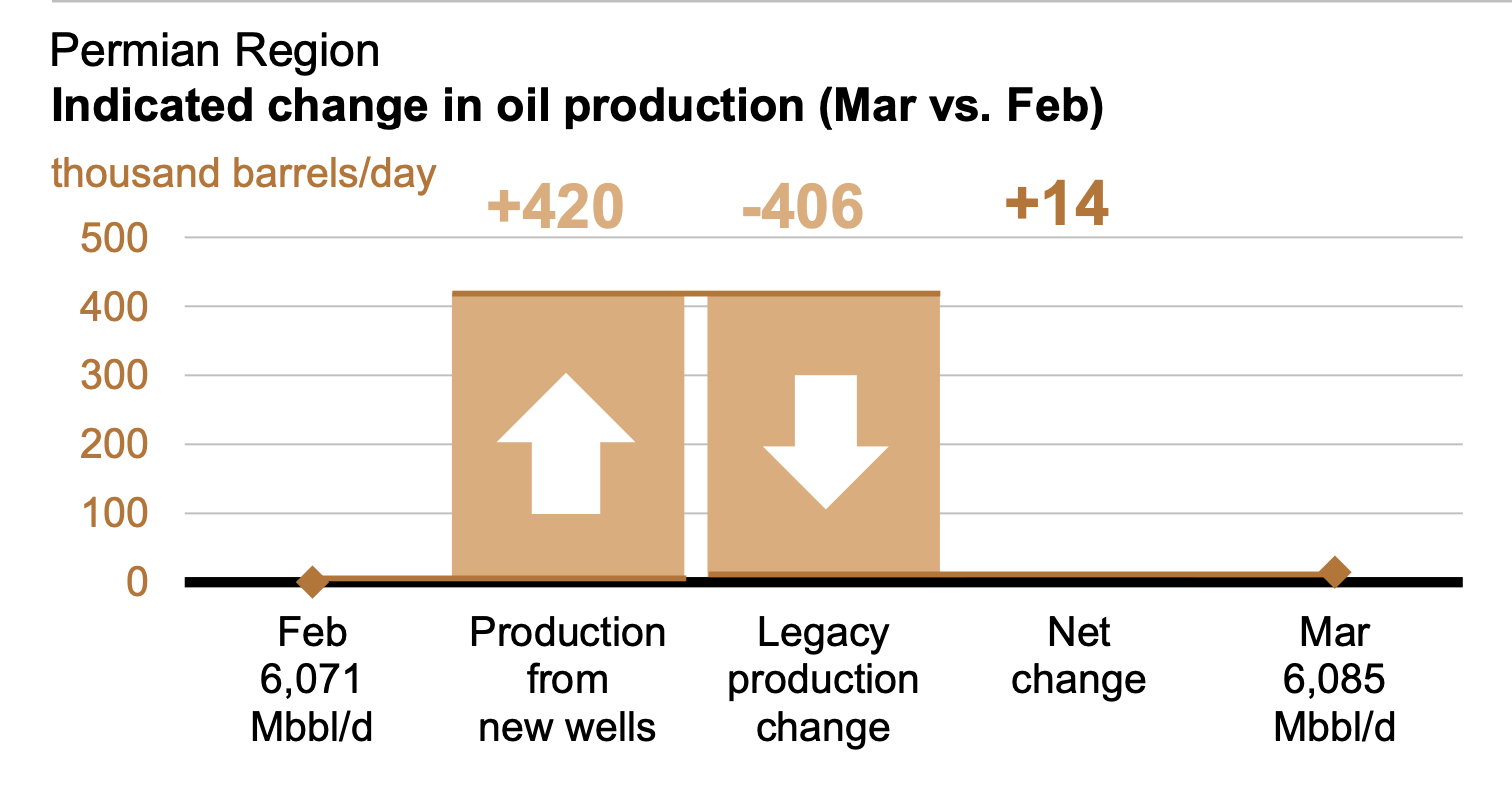

Are there some short-term advantages to Exxon being able to implement these technologies? Yes. Longer wells and cube development (when done right) increase initial well production. But faster initial oil production from shale oil wells also means faster declines as these technologies don't get more oil out of the ground, they just get the same oil out faster. One thing that is true about shale oil development is the equation always balances. The current technology gets a certain amount of oil out of the shale. If you take it out faster, it doesn’t make more oil, it just means you get more oil upfront and then faster declines. With the Permian already plateauing in production, the majority of new oil production in the field just goes to keep pace with declines of existing wells. Faster well declines will be another challenge facing the Permian in the very near future.

Source: EIA

Art Berman is a geologist and an oil industry analyst. A true oil man with a strong track record about being right about the U.S. shale industry. He wrote this about the Permian in January.

“The answer is that shale wells are producing at higher initial rates but are declining faster than in previous years. Their total recoveries are lower than just a few years ago. The wells are burning out. Oil supply—like life—is a marathon, not a sprint. The plays have been over-drilled and wells are interfering. They are cannibalizing production from each other.”

Can cube development and longer wells increase the combined acreage of Exxon and Pioneer from 1.3 million barrels per day to 2.0 million barrels per day by 2027 as Exxon CEO Darren Woods claims is possible? Highly unlikely. If this was 2011 and the Permian had never been drilled and fracked, this might be a different story. But it is 2024 and most of the best acreage in the Permian has been drilled. Often overdrilled — creating child wells — that then cannibalize production from existing wells, as Berman notes. I wrote about this short-term approach in 2018 in an article titled, “The Fracking Industry Is Cannibalizing Its Own Production.”

The problem with promising long wells and cube development as your solution to the Permian is that there isn’t room for a lot of that like there would have been in 2011. The acreage has been overdrilled. It’s good to remember what Scott Sheffield, the CEO of Pioneer Resource and soon to be Exxon board member said in March 2023, before Exxon was paying $60 billion for his company, “We just don’t have that potential to grow U.S. production ever again."

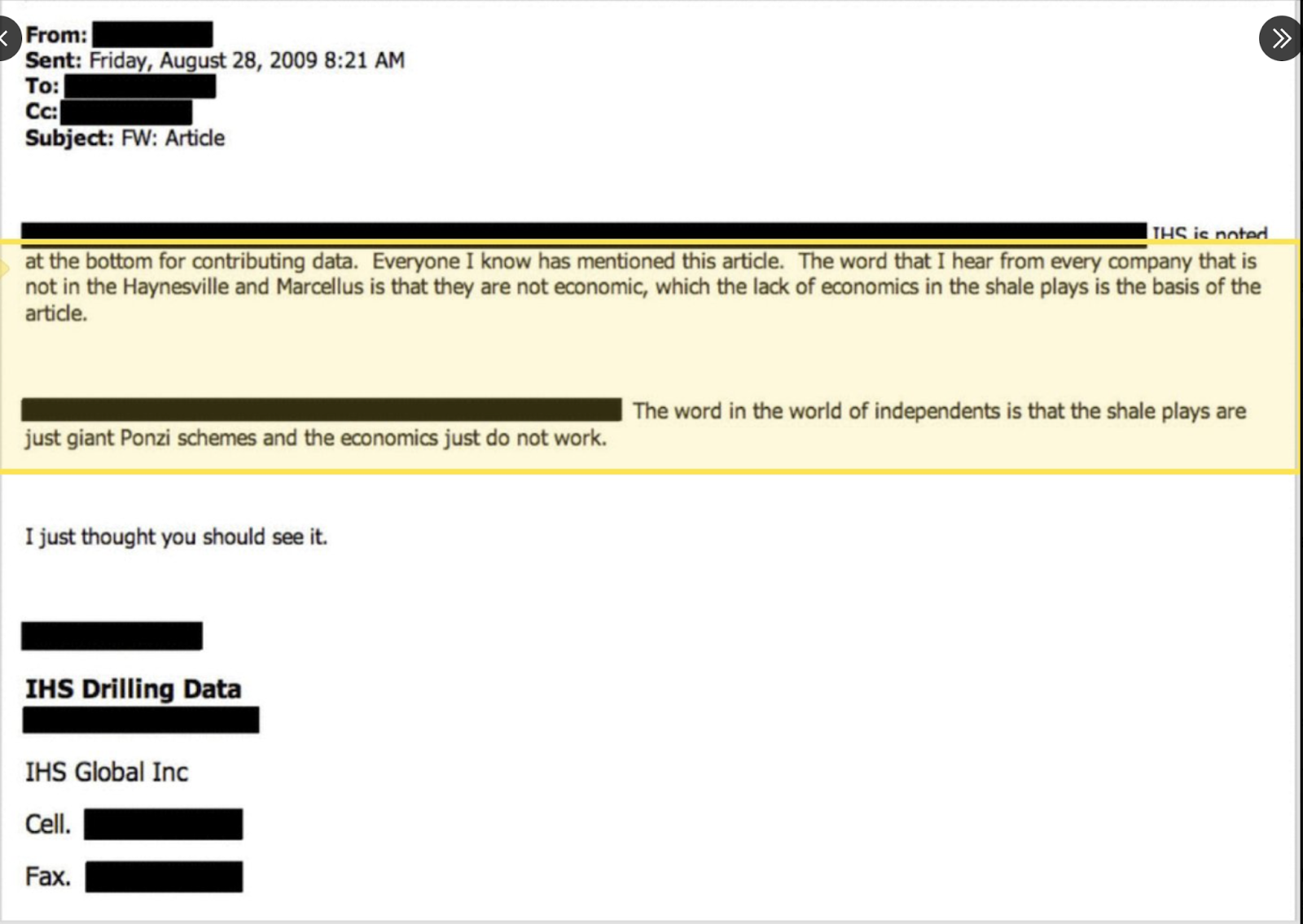

A favorite saying in the oil industry when trying to lure in more capital is “this time will be different.” But if you pay attention you can see it isn’t different. It’s the same old con. There is a reason that an email from an employee at prominent industry analysts IHS called the shale industry a Ponzi scheme all the way back in 2011.

Image Credit: New York Times

The Critical Question

In February Reuters industry analyst John Kemp wrote about efficiency gains in the U.S. shale industry and noted that “The critical question is how much longer efficiency gains can keep driving significant output growth without an increase in prices and drilling.”

Irina Slav referenced Kemp’s piece in her analysis for Oilprice.com and made a very important point about where the oil industry is at with its current technology.

“[T]here is still plenty of crude untapped in the U.S., but tapping it requires a certain price level that hasn’t yet been reached. In short: dripping sweet spots are running out. At some point, drillers will need either higher prices or lower output.”

It seems in the oil industry, for everyone who hasn’t recently spent $60 billion to acquire Permian acreage, there is growing acceptance of the fact that the U.S. is not running out of oil and never will — but it certainly is running out of “sweet spots” that allow for it to be produced with a chance at a profit.

The Permian is likely peaking as economic oil resources become scarce. And it will very likely follow the same curves as the Eagle Ford and the Bakken which are both well below peak production. Those two plays began developing before the Permian and thus got to peak production sooner.

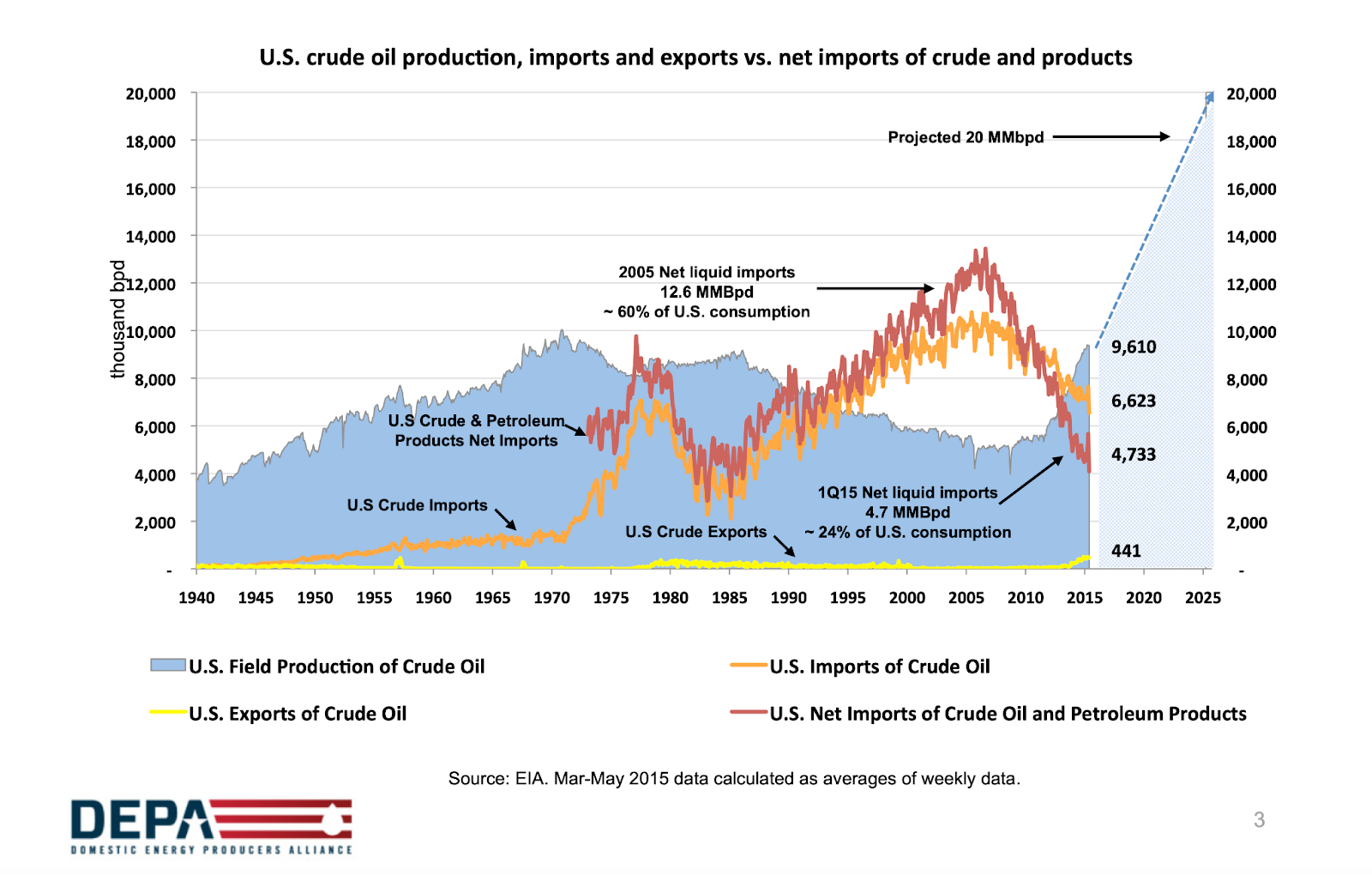

Harold Hamm is the king of Bakken shale and owner of North Dakota’s top oil company, Continental Resources. He used to make highly optimistic predictions of future production possibilities for shale production. In 2015, while successfully lobbying for the lifting of the U.S. crude oil export ban, he showed a slide with a graph estimating 20 million barrels per day of oil by 2025.

Source: Domestic Energy Producers Alliance

A few years of declining production in the Bakken seems to have brought him back to reality and in November Bloomberg reported that Hamm is conceding that the glory days of shale are over and it was time to move on to the next phase of the industry where new technologies will be needed to deal with less productive shale.

According to Bloomberg, Hamm said, “a new wave of inventions will be needed to make Generation 3 rock productive” and that “...more extensive development will require new technologies, and to maintain industry profitability amid elevated inflation, oil will have to trade at $75 to $85 per barrel.”

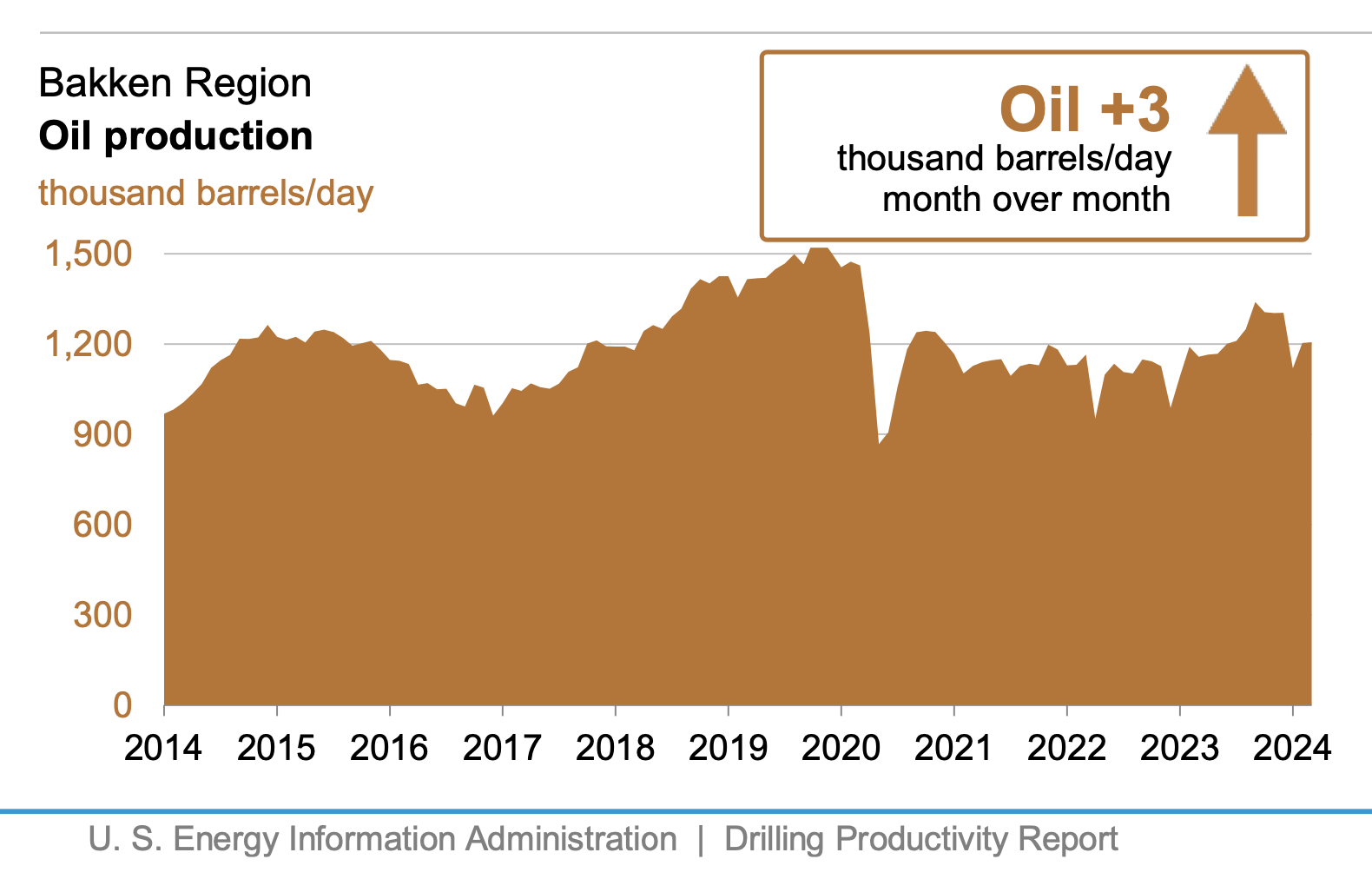

If you are interested in the future of the Permian, the current state of the Bakken might be a good estimate.

Source: EIA

It’s not like they aren’t trying in the Bakken. In December, North Dakota reached a new record for the number of wells in production and still total oil production fell by 6,000 barrels a day.

While there is the possibility that there could be “new inventions” or “very dramatic new technical innovation” that make producing shale oil from the remaining shale acreage in the U.S. profitable, that is far from a given. It is also possible that the nuclear fusion industry will have the same luck. Or the carbon capture industry. My advice, don’t bet on any of it.

Powering the Planet is reader supported. Please consider subscribing.

Comments ()