The End of the U.S. LNG Bubble

For the U.S. LNG industry to make money it will require many factors all to align in the "Goldilocks Window" and that outcome is highly unlikely.

In 2019 I wrote an article making some predictions for how the U.S. energy markets would play out and it was titled, “The Inevitable Death of Natural Gas as a ‘Bridge Fuel’ which included this prediction.

“... if all of the planned infrastructure gets built to export U.S. natural gas in liquid form (known as liquefied natural gas, or LNG), prices for natural gas are very likely to rise. This is the industry’s survival plan for the future. However, the higher prices natural gas producers need possibly will kill off one of the industry’s main markets.”

Due to the fracking boom the U.S. was producing much more gas than it could use. Access to global markets was the only way to make a profit on producing natural gas in the U.S. which spurred the massive investment in U.S. LNG export terminals and now the situation has been reversed as the U.S. will be exporting so much gas in the form of LNG that the U.S. will have a gas shortage and domestic gas prices will rip higher. It’s already happening. From the Wall Street Journal:

"Electric bills are expected to keep climbing this summer along with the temperatures. The Energy Information Administration expects the average U.S. residential electric bill to be about 4% higher this summer than last, the largest source of power generation. Natural gas deliveries to power plants will cost about 50% more from June through September than last year."

The WSJ includes an explanation from an analyst on what is driving this.

“The more we export gas, the more the domestic price will begin to reflect the international price”

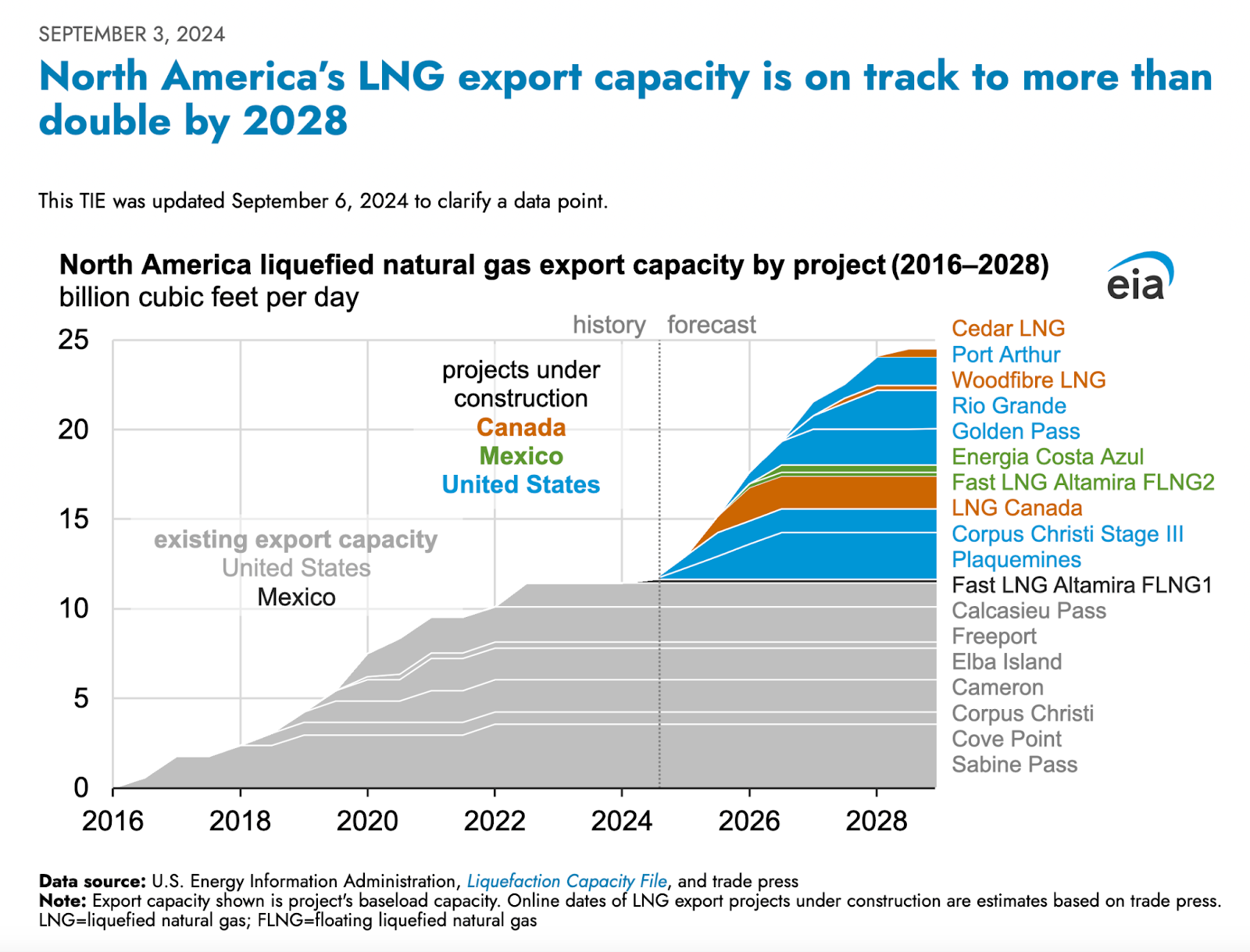

The companies exporting LNG from the U.S. will double their capacity by 2028.

International prices of gas are much higher than U.S. prices. If the U.S. government doesn’t step in to limit exports the U.S. public is going to be paying much higher prices for gas and electricity. This was easy to see coming. And now it is here.

But there is a catch for anyone expecting this means their U.S. LNG export investments are about to pay off. Actually, a couple.

The Simple Math

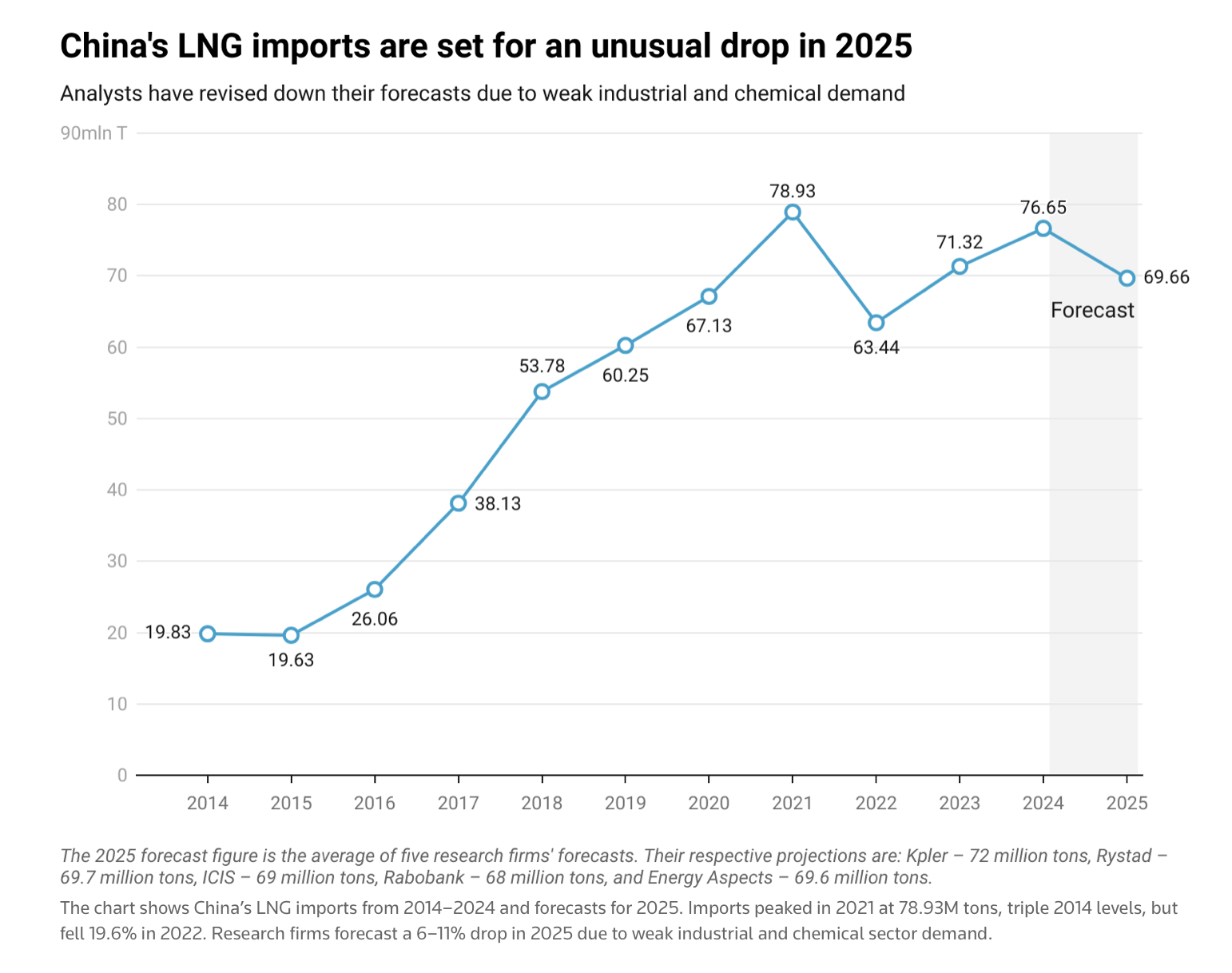

As I argued in 2019, what is happening now was inevitable. The price of natural gas in the U.S. had to go up because they were selling it for less than it cost to produce it. At the same time, the price of renewables was going to go a lot lower. And it has. While Republicans in America are trying to stop renewable energy and their leader says that “windmills are killing this country,” renewable energy is dominating around the globe. Producing electricity with renewables is much cheaper than importing LNG and burning it to produce electricity. Much cheaper. It is not close. Many analysts are still predicting strong LNG growth in China but they don’t mention a key aspect that showed up in an article last week about what is actually happening in China. Bloomberg noted how owners of Chinese gas power plants are asking the government to build a lot more gas power plants “in a bid to help prop up faltering demand.” What could be causing gas demand to falter? Economics. In this article they use the phrase “seaborne gas” to refer to LNG and the economic situation is quite clear in that case.

“Any potential buildout [of new gas power plants] still faces major hurdles. Seaborne gas imports are prohibitively expensive compared to domestic coal or renewable sources.”

Prohibitively expensive in what was supposed to be the largest growth market for LNG. To see what happens when your product is prohibitively expensive compared to the competition, here is a graph from Reuters on China’s LNG imports.

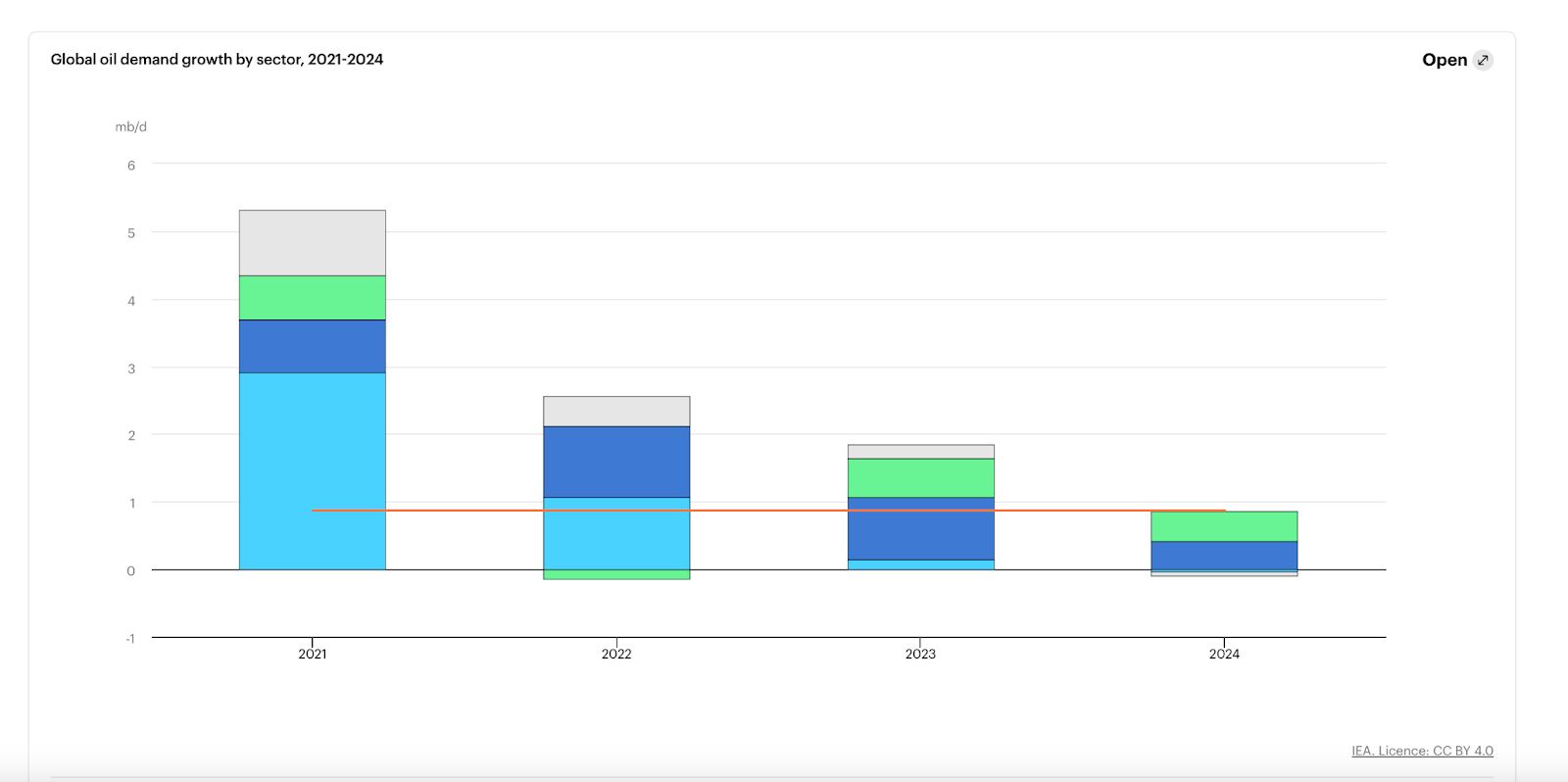

The timing of this is really quite remarkable. Hundreds of billions of dollars are being spent to build new LNG export terminals around the world. LNG is the oil and gas industry’s last stand. Every major oil and gas company is making big plans for LNG sales in the future. Why? The graph below of global oil demand growth explains why. If they can’t talk about LNG growth to their investors, there is no growth to talk about other than their plans to make more plastic, which also aren’t going as well as they expected.

Global oil demand growth 2021-2024

Source: IEA

However, there is no turning back from this policy now. U.S. domestic gas prices will go much higher as a result of the LNG exports. That is locked in. So, higher U.S. natural gas prices are good for the U.S. LNG industry right? This is one of major catches(and perhaps fatal economic flaw) facing the U.S. LNG industry.

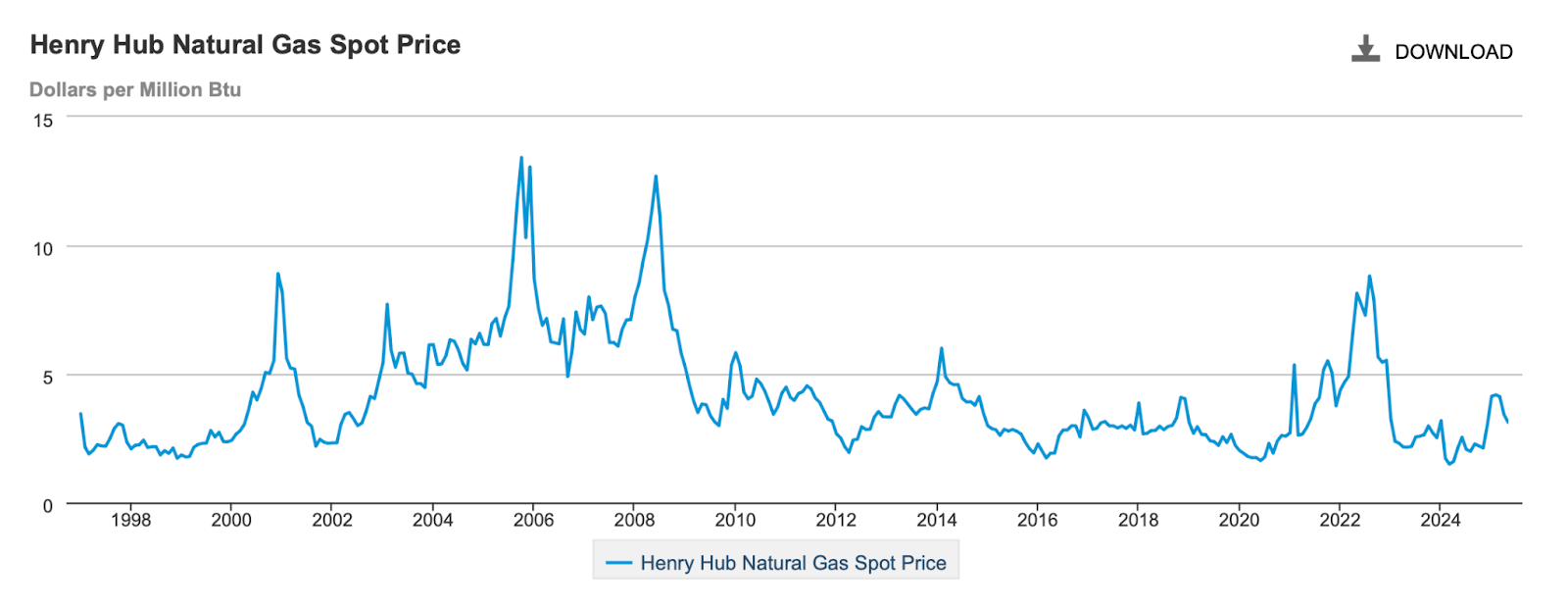

The Henry Hub-Indexed Feed Gas Problem

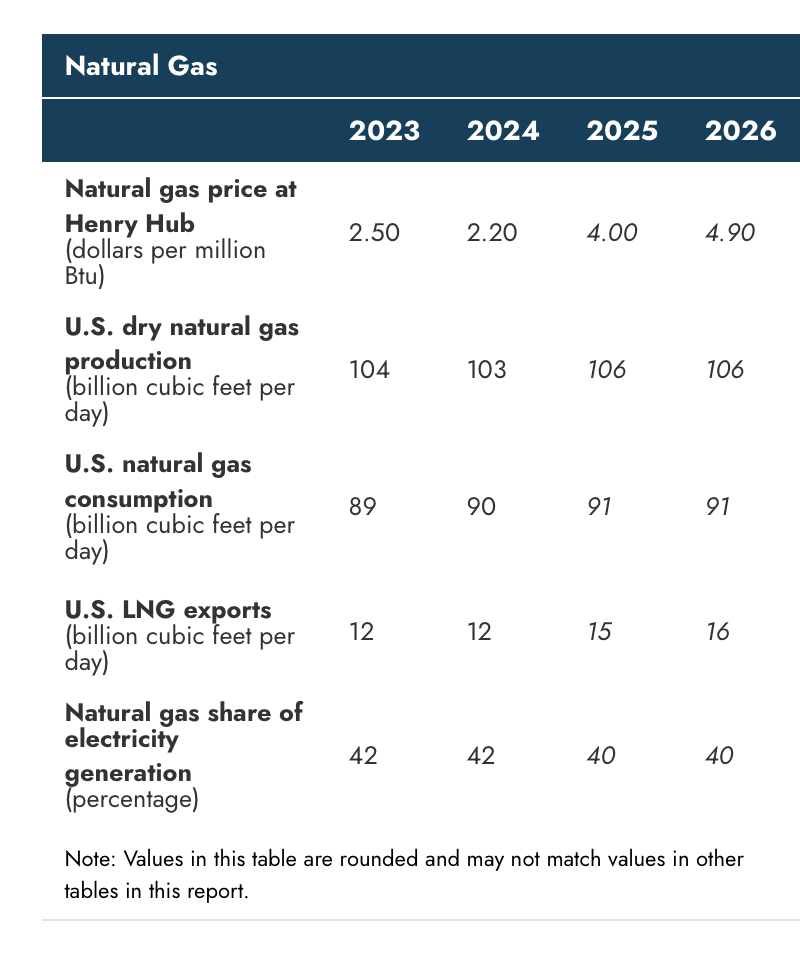

Most of the LNG sold on long-term contracts from the U.S. is based on the price of natural gas in the U.S., which is referred to as Henry Hub pricing. Here is a graph of the historical prices for Henry Hub gas.

Source: EIA

The impact of the shale boom is pretty clear. In the decade prior to 2010, Henry Hub gas pricing was often $5 or much higher. Then the flood of fracked gas showed up and there was too much and prices dropped and stayed low as supply was greater than demand. The big price spike in 2022 was due to the Russian invasion of Ukraine. However, that waned and prices returned to very low levels until the second half of 2024. The U.S. gas producer industry’s plan is to drive up U.S. gas prices by increasing demand with LNG exports. And it is working. Look at the EIA predictions for Henry Hub prices in 2026.

Source: EIA

Average price in 2024: $2.20. In 2026: $4.90. I won’t be surprised if it goes higher than that in 2026 (Earlier this month when I started writing this piece the EIA was saying $4.80 but it has since been bumped higher). The unique thing about U.S. LNG contracts is that they are indexed to Henry Hub pricing. Traditionally LNG contracts were “oil indexed” which means the prices of the LNG was based on the price of oil. This 2019 article notes how the emerging U.S. LNG industry was facing challenges trying to get buyers to index the price of LNG to Henry Hub pricing. The article explains the basic concept of US LNG contracts for the top US LNG exporter.

“For example, Cheniere’s long-term sales and purchase agreements (SPA) reflect a purchase price for LNG that is indexed to the monthly Henry Hub price, plus a fee.”

“The price of Henry Hub-indexed LNG is typically structured as HH + 15% multiplier + liquefaction fee + shipping costs.”

This was seen as a real advantage for U.S. LNG exporters at the height of the shale boom when we were being told that there was an endless supply of cheap oil and gas in U.S. shale (It was also when I wrote my first article about the coming peak in U.S. shale). In a 2017 Wall Street Journal article titled, “Henry Hub Emerges as Global Natural Gas Benchmark” the head of global energy at CME, one of the world's largest operators of financial derivatives exchanges(they make money off of people trading things, like LNG), said this:

“The U.S. is going to be the price setter for majority of the freely traded market,” said Peter Keavey, global head of energy at CME. “You’re exporting the Henry Hub benchmark to the rest of the world." In that same article Spencer Dale, chief economist at BP PLC stated that, “The economics suggest that U.S. gas prices will act as a natural anchor [for global LNG prices]”

Six years later I would argue that Dale was very accurate with the use of the word “anchor” when referring to U.S. natural gas prices. They are going to drag down the U.S. LNG industry. The people betting on shale gas prices remaining where they were during the peak of the U.S. shale boom have made a very big mistake.

Buyers of U.S. LNG typically have contracts like those explained above which mean if the price of Henry Hub gas goes up, the price of their LNG goes up. The costs are passed through to the buyer. So, for the various parties involved in the LNG trade, increasing Henry Hub prices have very different impacts.

U.S. gas producer: Higher Henry Hub prices means actual profits for U.S. gas producers. They have been and continue to be huge advocates of LNG exports. It makes perfect sense for them as all they care about is profits and if they have to make electricity and heating really expensive for Americans to make those profits…they don’t care about that.

U.S. gas exporters: Henry Hub is their feed gas pricing. Higher Henry Hub prices are passed through to buyers so not a problem as long as they can find buyers which was easy to do when Henry Hub was $2. It won’t be easy at $5.

Buyers of US LNG exports: Very unhappy with this situation as when Henry Hub goes up in price, they pay.

This helps explain why there isn’t much demand for long-term contracts for U.S. LNG at this point. Remember the article from 2019 which pointed out that most LNG in the world is indexed to oil prices? If you had your choice of an oil indexed contract right now or an Henry Hub indexed contract, you are going to strongly consider oil indexed. Why? Because when wars aren’t bumping up the global price of oil, the price is expected to be headed down as there is a global oil glut (remember that graph above about the declining growth in global oil demand). So, oil prices are expected to go down while Henry Hub prices go up. This is a problem for the U.S. LNG industry. An industry that already had a problem with economics before this situation arrived. It has been reported that U.S. LNG exporter Venture Global is trying to renegotiate existing LNG contracts higher – trying to convince their customers to agree to pay more for LNG as they can’t make the numbers work otherwise. Meanwhile, an Australian LNG contract with China was recently re-negotiated down with leading LNG energy analyst Seb Kennedy estimating the discount was $1 billion over five years. Which makes sense when you see the graph above about the direction of China’s LNG exports. To put that number in perspective, in 2024 Venture Global had a net income of $1.5 billion.

The world is facing a global LNG supply glut. Global LNG prices will get cheaper. It will be a buyers market. Which means, if you are selling LNG indexed to Henry Hub pricing, you have a problem. In January the Oxford Institute for Energy Studies released an analysis of the future LNG market. Their high cost assumption for HH pricing through 2050 is $4.62 where they say, “with Henry Hub at $4.62 per MMBTU in 2050, the margins are very tight, suggesting that a lot of U.S. LNG would simply be shut-in.” So what happens when it is $5 next year? In the recent Argus Media piece titled, “US gas market expected to tighten in 2026” oil and gas industry financing gurus and investment bankers say they expect the U.S. gas market to be in a state of “material undersupply” in 2026. What do these money people think this will do to the U.S. markets? The same as I do, saying that undersupply could, “potentially pushing domestic prices so high that the price of producing LNG from US gas would exceed prevailing global LNG prices.” Now, go back up to the chart above that shows how much more supply will be added to the U.S. LNG export capacity between 2026 and 2028. There will be blood.

That Argus piece also included a more optimistic view from another analyst saying, “Henry Hub prices would probably have to exceed $7/mmBtu given current global gas prices for US LNG cargoes to start being cancelled.”

Anyone investing in new US LNG export projects is going to lose a lot of money. However, the huge LNG investment boom we were promised when the Biden administration shuffled out of D.C. has not happened. Perhaps the last of the dumb money was all used up on New Fortress Energy and Venture Global?

Seb Kennedy at EnergyFlux recently summed up the reality for U.S. LNG and its Henry Hub indexed business model saying, “Combined with an enduringly soft oil market, selling US LNG in Asia is about to become a tough gig.” The Financial Times ran a piece this week on how the global oil industry was now a sunset industry. Something I wrote about a year ago. Sunset industries are expected to be “enduringly soft.”

The Supply Problem

We are told the U.S. gas market could be in material undersupply by 2026. I’ve explained all of the details of why that will happen in this piece so I won’t rehash that here. The quick summary is that the U.S. no longer has the ability to supply markets with ridiculously cheap natural gas. U.S. oil production has peaked and that is bad news for U.S. gas production as much of the growth in U.S. gas has been the associated gas that comes out of the ground with fracked shale oil. However, the U.S. has not run out of shale oil to frack and extract, it is just that the stuff that is left costs a lot more to get out of the ground then the market is willing to pay. Same story for U.S. gas. There is gas in the shale of Haynesville which is conveniently located very close to the U.S. export terminals on the Gulf coast. However, it is inconveniently located much deeper underground than most of the gas currently being produced which makes it very expensive to extract. How expensive? $5 to start. To start. From Reuters:

“Gas futures will need to stabilize around $5.00 through 2027 before large gas producers have an incentive to ramp up production, said Kevin MacCurdy, managing director at Pickering Energy Partners.”

It does not appear that there will be any difficulty with U.S. gas prices stabilizing at or above $5 by 2027. In addition to the massive ramp up in LNG exports, have you heard about datacenters and AI and the plans to build huge numbers of new gas power plants to power chat bots? More demand. Remember what happens to the U.S. LNG export business when Henry Hub pricing gets over $5. Can the Haynesville deliver big volumes of gas at that price? Maybe. However, that is the best case scenario. And it is setting up a very small Goldilocks Window in the U.S. LNG market. To keep U.S. LNG competitive on the global markets all that is needed is for the Haynesville to produce lots of gas at $5. However, if oil prices stay lower for longer (which will happen unless the wars get out of control at which point no one will be worried much about LNG pricing) then even $5 Henry Hub pricing might make U.S. LNG too expensive for global markets. At $7 Henry Hub the Haynesville will be rocking….except there will be no market for $7 gas as there will be no LNG export business.

Timera Energy wrote a piece called “What Happens to LNG Market if Henry Hub Rises" and concluded that:

“If US netback LNG prices decline below the variable production cost of export terminals, there are huge volumes of cargo cancellation potential (as liquefaction capacity is ‘shut in’ and export gas volumes sold back into the domestic market).’

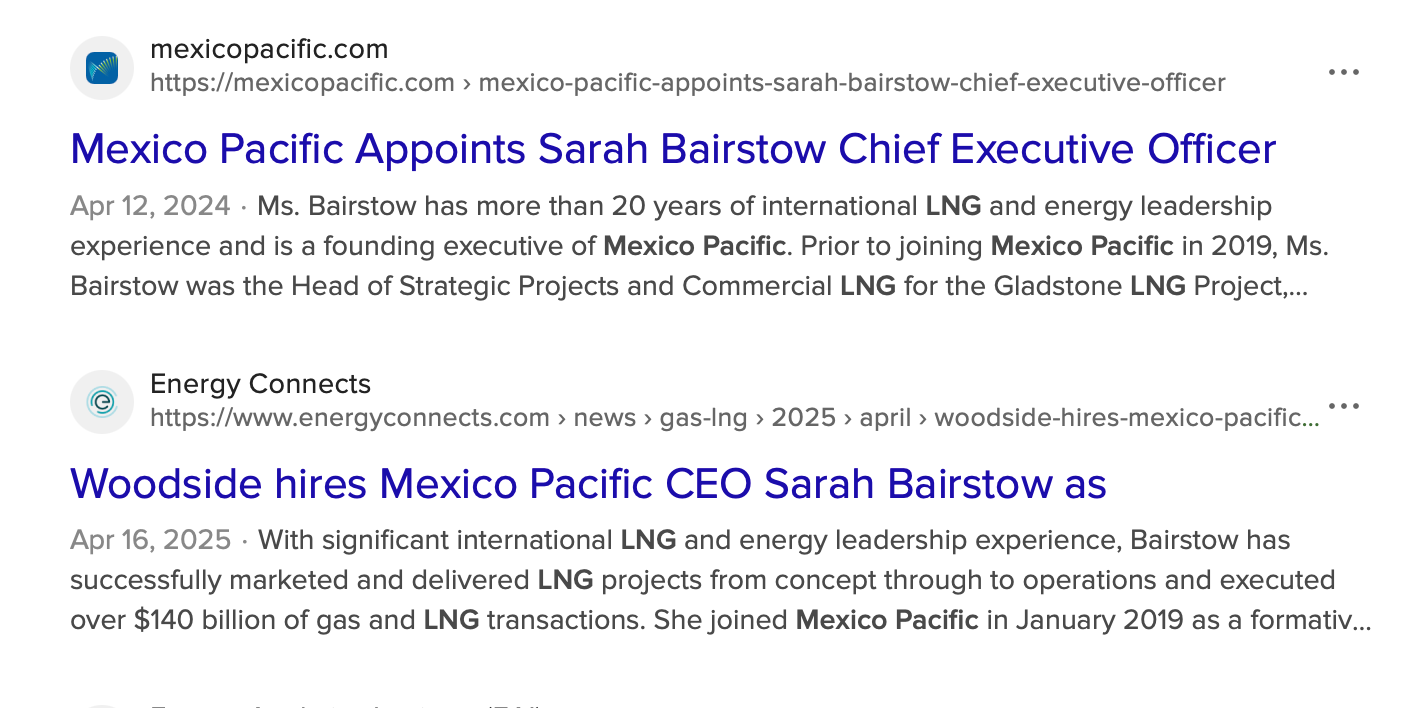

The U.S. LNG business has a big supply problem. It will only get worse. Were you thinking of getting Permian gas for your big LNG export facility in Mexico? Really? There is a good reason the CEO of that proposed project quit recently. You can see the timeline of her career choices in this image. She spent a year on the project and got out. She understands the simple math.

The Debt Problem

The bankers that loaned money to fund the shale boom lost a lot of money making loans to people who couldn’t pay them back. Well, the bankers got rich making the loans, other people lost money because they listened to the banker’s advice. Remember when Goldman Sachs told everyone that U.S. LNG exporter Venture Global’s IPO was a great investment? If you listened to them you lost a lot of money. Fast.

It’s the same mentality and business model that drove the U.S. housing crash in 2008. And they aren’t going to change something that makes them very rich. And so they have been happy to load up U.S. LNG companies with debt. New Fortress Energy lost money the last two quarters. The company is currently valued at about $600 million. It has $9 billion in debt. The math isn’t hard and New Fortress is expected to declare bankruptcy soon after Fitch recently downgraded its credit rating. As part of that analysis Fitch stated the following (which is not what you want to hear if you own Venture Global shares): “NFE is closest in operations and geographical focus to LNG producer Venture Global LNG, Inc.”

Fitch says the following about Venture Global: “VGLNG's [Venture Global] two operating projects have substantial leverage, which could limit cash flows at the parent if merchant prices were weaker.” Substantial leverage. Venture has over $30 billion in debt and is making plans for a lot more to expand their LNG export capacity.

One thing to note about the dire picture Fitch paints for these two companies. Fitch makes some bizarre assumptions about Henry Hub pricing for 2026 and 2027 with estimates of $3.00/mcf in 2026 and $2.75/mcf in 2027. Those are about the most favorable assumptions you could make for these two companies. It is highly likely actual prices will be much higher. That will be bad for companies, like Venture, who have what Fitch calls “substantial leverage” aka debt.

The Global Demand Myth

The U.S. LNG business model is not competitive on the long-term global market for several reasons. However, the global LNG market also has a problem that is not specifically associated with the U.S: the demand isn’t there.

Wood MacKenzie are big supporters of the U.S. oil and gas industry. They make their money that way. But even they can't avoid the stark reality of what is revealed when you do some simple math.

"With LNG demand growth slowing after 2030, there is an increased risk that US LNG cargo cancellations might be required to balance the market, particularly in 2030-32."

Remember this is the same group that recently put out an “analysis” that claimed LNG emissions were much lower than those for coal. It was not peer-reviewed. It did not mention all of the new satellite data on methane emissions that make its claims highly unlikely. So they are optimists about how LNG demand growth could slow after 2030. Meanwhile, it is slowing now.

As noted above, China’s LNG imports are significantly lower than last year at this time and are expected to be lower for the full year. One reason why is the large increase in renewable power generation in China is causing power prices to “nosedive” and this article explains that is due to ‘A crash in Chinese coal prices and a flood of clean energy are cutting power rates in major industrial hubs, easing pressure on some of the factories caught in the crossfire of trade hostilities with the US.”

India

I’ve written in detail about why it is unlikely for India to ramp up LNG exports like we are being assured will happen and my main argument is that LNG is far too expensive for India to adopt widely when solar plus storage is faster and much cheaper. This Reuters article on the steep drop in coal use in India makes it clear how this is playing out.

“Natural gas-fired power generation [in India] fell 46.5% annually to 2.78 billion kWh in May, the steepest decline since October 2022.”

Why?

“Meanwhile, renewable energy output surged to a record high of 24.7 billion kWh in May, up 17.2% from a year earlier”

Cheaper wins.

Pakistan

Pakistan is rapidly building out solar and storage. LNG imports declined over the second half of 2024 for Pakistan and, like China recently did, they also would like to renegotiate one of their long-term LNG deals…. lower.

Thailand

BNEF released an analysis in May where the title sums up the reality: Solar, Wind and Batteries Could Enable Thailand to Reduce Reliance on LNG Imports. Why?“solar power has been the cheapest source of electricity generation in Thailand since 2022” and “Solar paired with batteries has already become more economically viable than newly built gas- and coal-fired power plants.”

Europe

Europe’s LNG imports declined almost 20% in 2024.

South Korea

A new report by IEEFA sums up the situation in South Korea

“given declining domestic demand, high costs, and existing long-term contracts, relying on LNG is unlikely to be an economically feasible solution for South Korea.”

Latin America

Natural Gas Intelligence reports on Latin American LNG demand recently going way down.

"Imports into Latin America are predicted to reach 0.29 million tons (Mt) in June, down from 1.37 Mt in June 2024. Last month’s imports also were down on a year/year basis to 1.13 Mt versus 1.45 Mt in May 2024, according to Kpler."

One can start to see a trend.

US LNG is Dirty

Last year I wrote about how the efforts to sell the world on the lie that LNG was "clean" and "low emissions" were going strong but that the science shows just how big a lie it takes to make that effort.

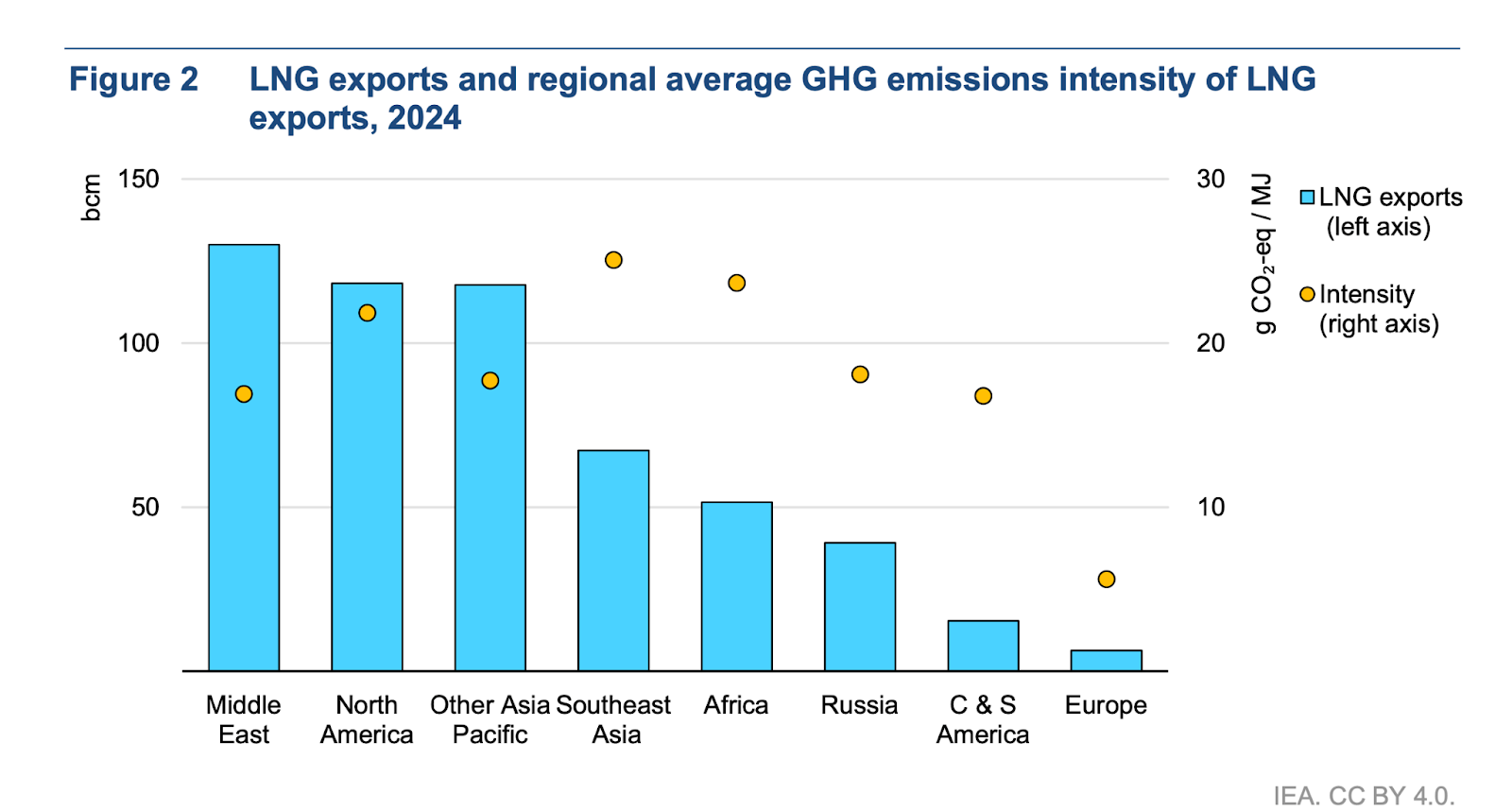

The EU is currently trying to figure out how it can lie to the world and say that U.S. LNG has low enough methane emissions to meet their standards. It does not. It isn’t even close. The International Energy Agency released a new report on LNG emissions last week. It makes many very favorable assumptions to try to make LNG look better. Even with all of that they still can only claim that LNG emissions are slightly lower than coal, which we all know are horrible. However, they also can’t hide the fact that fracked U.S. shale gas has very high methane emissions which means, as this chart shows, that U.S. LNG (North America) has some of the highest methane emissions in the world (the yellow dots show the level of emissions associated with LNG by region). Highest prices, some of the highest emissions. Not a great sales pitch.

Batteries Changed the Game This Year

It took me a while to write this piece and while it did another war broke out. Perhaps the world will see much higher oil and gas prices thanks to this war. War is always very good for the oil and gas CEOs. However, other news came out during the writing of this piece that really makes the rest of what I wrote here unnecessary.

From Reuters:

“Renewable power like solar and onshore wind is the least expensive and quickest power generation source to deploy in the United States, even without government subsidies, Lazard said in a report on Monday.”

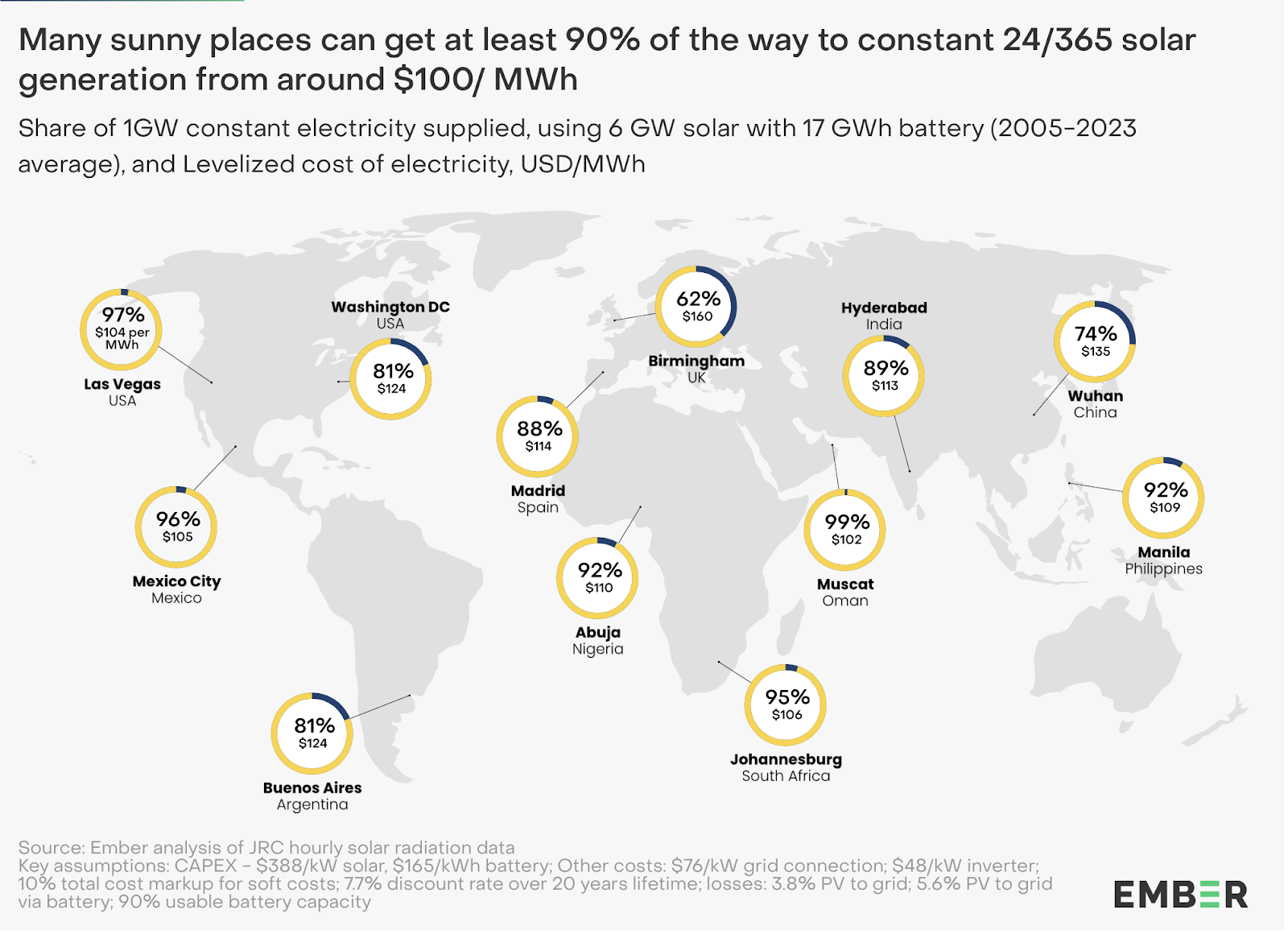

But the simple reason why the U.S. LNG industry (and fossil fuel power production in general) is in serious trouble is explained in this new report by the clean energy analytics group Ember. Due to the rapid fall in battery costs, it is now possible to pair batteries with solar and have it be cheaper than new fossil fuel power plants for 24/7 power supply.

Low cost wins. And, lucky for the world, low cost is also currently very very low emissions. Meanwhile, LNG’s sales pitch is, “really high costs and really high emissions.”

Do the math.

Comments ()