Supply and Demand Destruction

The energy markets are causing a lot of head-scratching these days. Why aren’t oil prices higher? What aren’t natural gas prices higher? What is going on with U.S. shale gas being so cheap? Will oil demand growth recover from these oil and gas wars or will it kick the energy transition into overdrive and will oil demand growth be a thing of the past? I’m confident no one really knows the answers to all of this but if you are in the oil and gas business it has to be unsettling. Sure you are rolling in the war profits now but if demand growth is a thing of the past, so are your future profits.

Ed Ballard at the Wall Street Journal wrote a piece this week about demand destruction.

“If you read about the economic fallout from the Iran war, you’ll encounter an ominous phrase: demand destruction.”

Ed makes great points and it is highly likely that if the situation in Iran is ever resolved and oil prices return to $50 a barrel, some of that oil demand currently disappearing will recover. However, the piece does quote the head of Saudi Aramco saying, “We don’t see any demand destruction.” I bet they don’t. Because if that demand destruction is real (some of it most definitely is and was happening anyway ) then the Kingdom of Saudi Arabia has a very big problem. Demand destruction means lower oil prices. The Kingdom needs oil prices around $90 a barrel to balance the Kingdom’s budget. Did you see they cancelled their pro golf league? Maybe they need the money to invest in all of that battery storage they are building?

The Saudi Aramco princes have been so wrong about their forecasts for so long that hearing them say they don’t see demand destruction likely means there is even more demand destruction than most people think. I expect it will take a couple of years to figure that out but in 2026, global oil demand is very likely going to be less than in 2025. They weren’t expecting that. OPEC’s forecasting is so overly-optimistic that in December of last year they were forecasting global oil demand of 1.3 million bpd for 2025. The actual number for 2025 was 850,000 bpd. So it’s wise to ignore anything the Saudis say about oil demand growth. This was what they said in December 2025.

“OPEC keeps its assessment of global oil demand growth unchanged, holding its outlook at 1.3 mb/d year-on-year for 2025 and about 1.4 mb/d for 2026.”

They were also wrong about 2026. IEA is now saying they expect 420,000 bpd of demand destruction in 2026 (almost 2 million bpd less than what the Saudi's predicted in December). It’s early in the year and eventually markets will have to come to grips with the reality of Hormuz and its impacts which are out there waiting for us. That demand number could certainly go lower.

So, oil demand destruction is happening and nothing the Saudi’s can say will change that. Did global oil demand peak in early 2026? Possibly. Either way, the IEA’s prediction last year (after the U.S. threatened to pull their funding) that oil demand growth would continue increasing until 2050 is not looking good. We will know a lot more about how quickly the world is moving away from oil in the next few years. However, when it comes to natural gas use, while there is a lot of confusion about global prices and U.S. domestic prices, there was real demand destruction happening before Trump and Netanyahu’s war and they now likely have sped that up with their fossil-fuelled fascism.

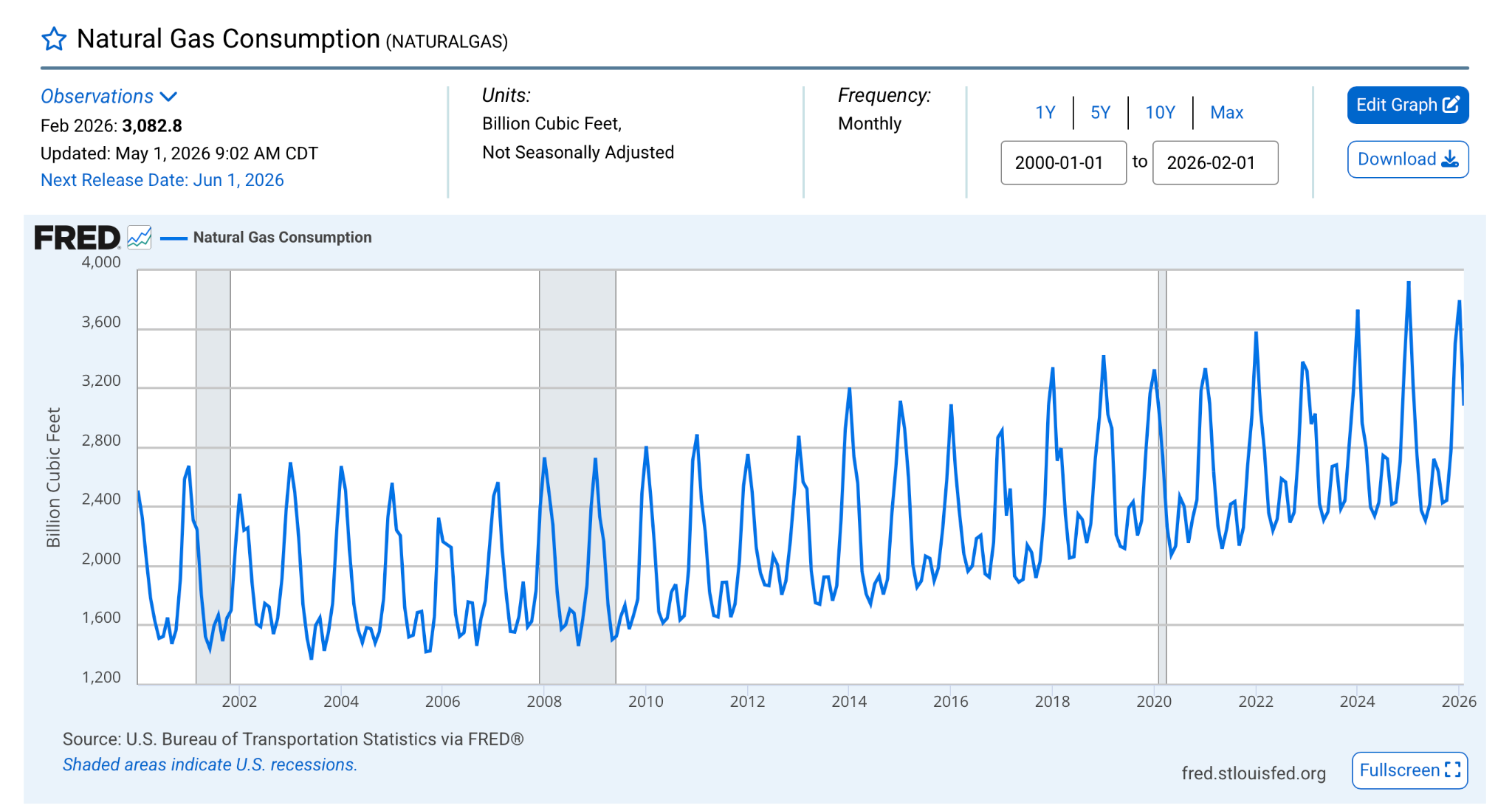

With all of the AI hype and the misinformation about renewable power that floods the media it isn’t surprising that people are wondering what is happening in U.S. natural gas markets. However, even for someone like me who follows this stuff every day, I am a bit surprised by what is happening in 2026. How are U.S. natural gas prices so low in this midst of a global natural gas crisis while U.S. natural gas exports are at record highs?

It appears the answer involves demand destruction which is coming from two sources that are both likely to accelerate – renewables plus storage and climate change.

US Domestic Gas Demand Destruction

In 2019 I wrote this.

“if all of the planned infrastructure gets built to export U.S. natural gas in liquid form (known as liquefied natural gas, or LNG), prices for natural gas are very likely to rise. This is the industry’s survival plan for the future.”

In 2025 I wrote this:

“The rapid development of the U.S. LNG industry was driven in large part by the bad economics of gas production in the U.S. after the shale boom. The U.S. was producing a lot more gas than it was using which cratered domestic gas prices. Much of the gas produced in the U.S. in the last decade has been sold for less than it cost to produce. Something had to change and LNG exports were the answer because they would drive supply shortages in the U.S and finally make the U.S. domestic gas industry profitable while also allowing LNG exporters to sell cheap U.S. gas to the rest of the world where the prices were much higher.”

This was the plan. U.S. gas producers need new markets for their gas. Right before the war I wrote an overview of the supply and demand situation for the U.S. gas market that explains the three main demand sources for U.S. natural gas - U.S. domestic demand, Mexican pipeline demand and LNG exports. Now we’ve been told that datacenters will drive huge U.S. gas demand growth. Possible. But it hasn’t yet and the early peak of natural gas consumption in 2026 was lower than 2025.

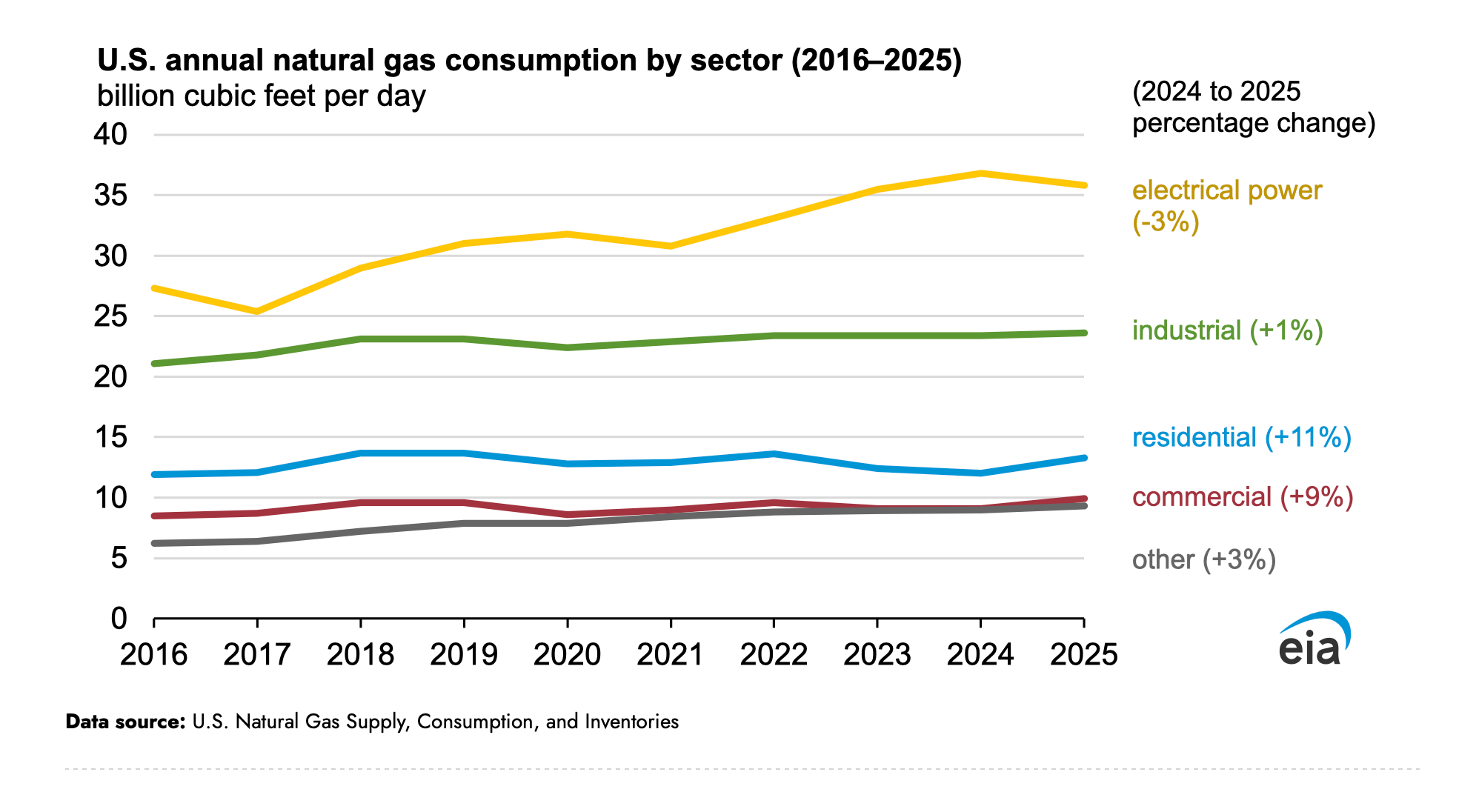

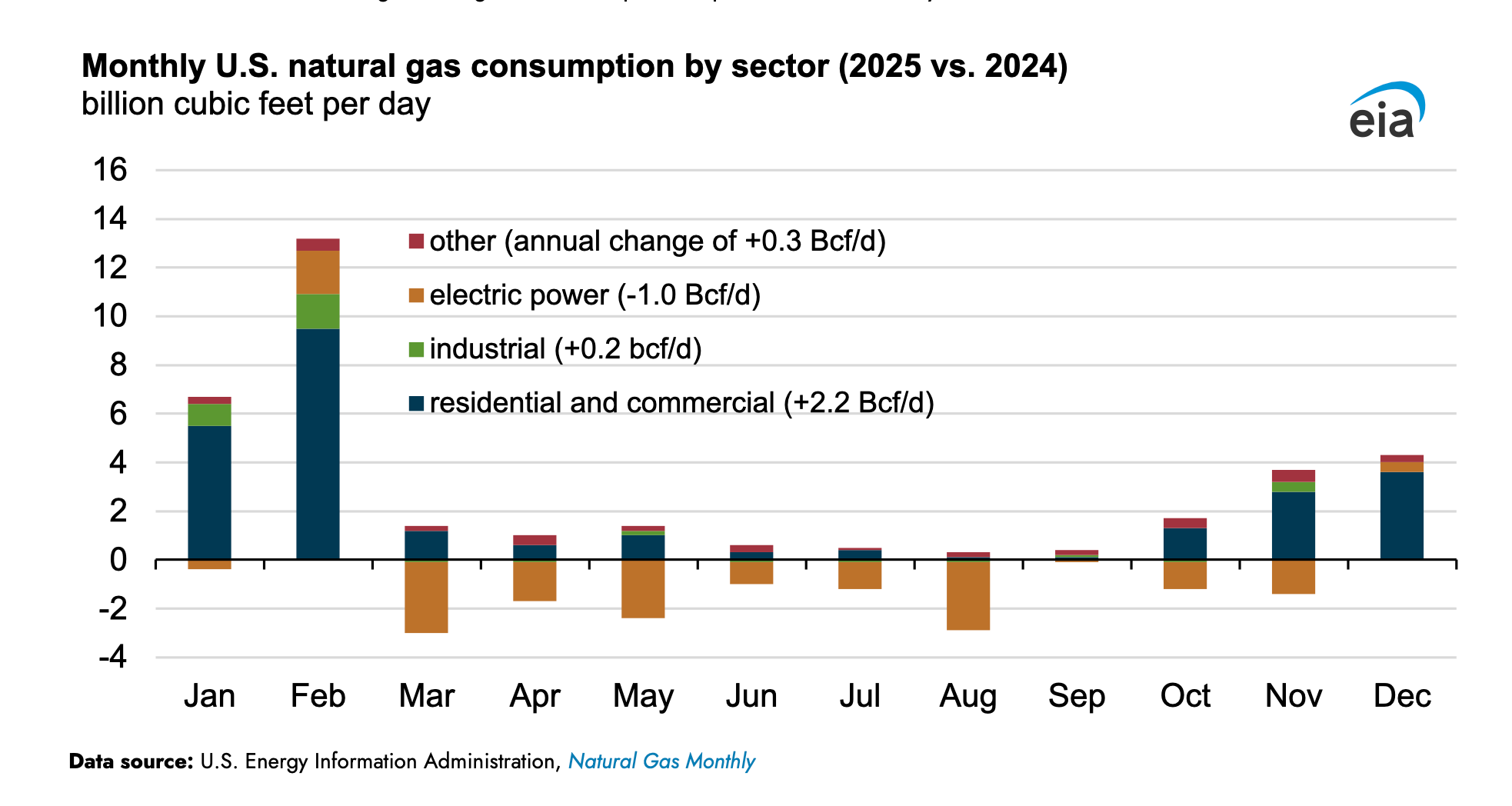

As noted above, the EIA can be quite optimistic in its forecasts for fossil fuel demand growth but do a good job of reporting reality on past use. They reported that U.S. domestic gas demand hit a new record in 2025 but that demand for power generation fell by three percent.

Why did this happen?

“The decline in electric power consumption of natural gas also reflected rapid solar and battery additions in 2025, which displaced natural gas-fired generation”

Displaced is another word for demand destruction in this case. How much demand destruction?

“Electric power use declined the most in March and August, by 2.9 Bcf/d and 2.8 Bcf/d, respectively.”

For a year that the U.S. exported 15 Bcf/d of natural gas as LNG, those are significant numbers. See all of those orange bars below zero on the graph below? That is what demand destruction looks like.

In late April of this year Natural Gas Intelligence reported the following stats:

“As of Saturday, year-to-date natural gas-fired power generation rose 0.6% to about 472 TWh, averaging 4,106 GWh/d, according to EIA-930 data.

Solar generation increased 19.7% year to date to about 85 TWh, or 734 GWh/d, while wind rose about 3% to 174 TWh. Coal-fired generation fell 10.7% to 211 TWh. Overall US generation edged up 0.2%”

Something is displacing coal generation and it isn’t gas, is it?

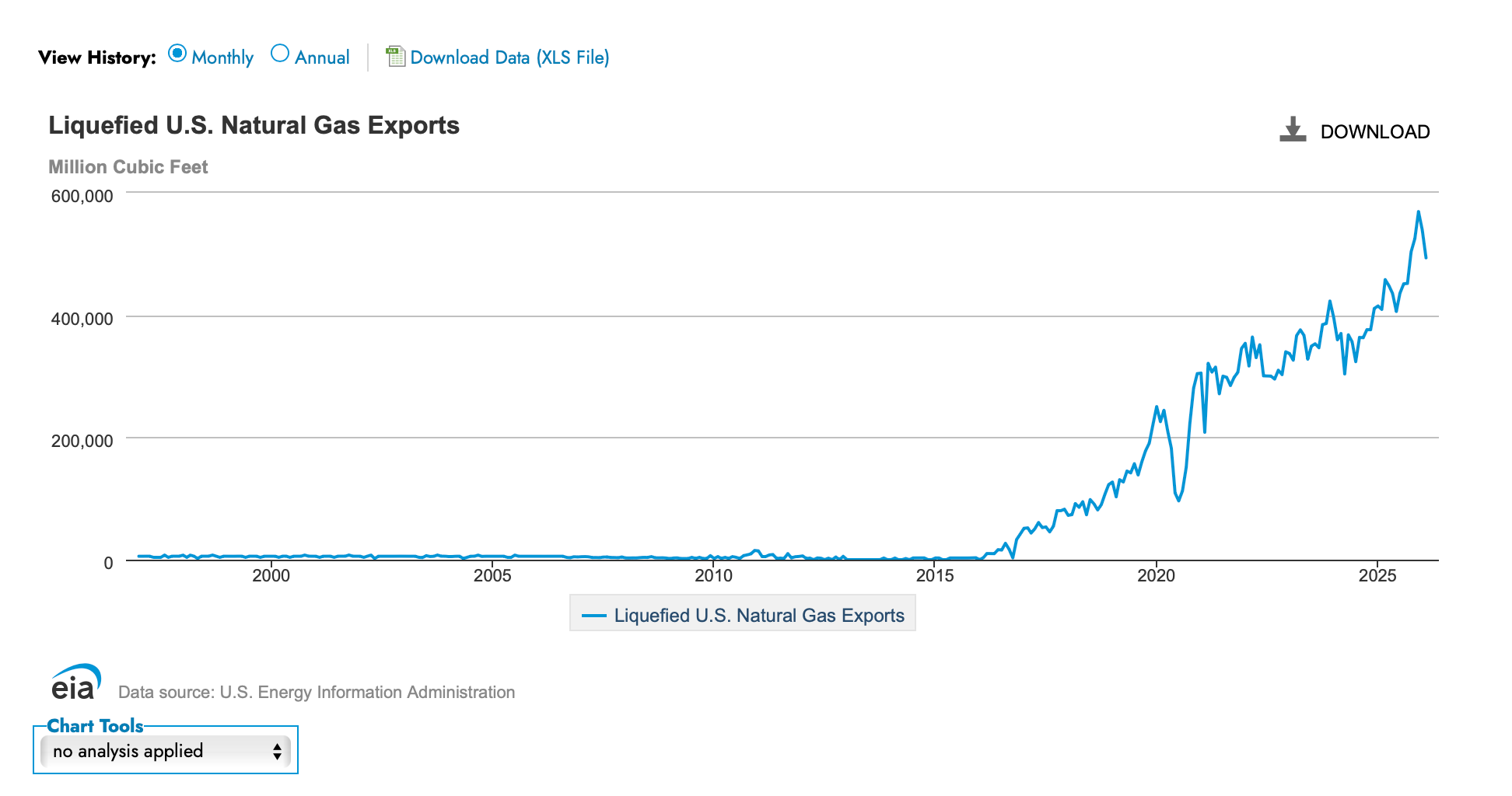

LNG exports growing rapidly

In 2024 the U.S. exported 11.9 billion cubic feet per day (bcf/d) of LNG. However, in 2025 the U.S. exported 15 Bcf/d. So LNG increased demand to fill the big demand drops in summer-month gas power generation. Their plan appeared to be working to create new demand for natural gas in global markets as U.S. demand decreased. And with new LNG capacity coming online including Exxon’s big Golden Pass facility, things appear promising for higher U.S. natural gas prices.

Last week we learned there was a drop in LNG exports from the records set earlier in the year (from a high of 18.8 Bbcf/d in April to 16.9 Bcf/d in May). The EIA forecasts that LNG exports should average just over 18 Bcf/d in 2027. So another 3 bcf/d higher than in 2025. This is expected to drive prices higher unless U.S. domestic gas use demand destruction continues.... as it very likely will. This will not be a smooth process and there likely will be price spikes in U.S. gas this winter. And as I’ve explained, if the U.S. builds all of the planned new LNG export facilities, it is highly likely to drive price increases in the U.S. as there are limits to how much natural gas the U.S. can produce and there is a good chance that demand could outstrip supply for a while. However, the big recent increases in LNG exports were expected to be driving price increases in 2026. And it isn’t happening yet.

Batteries are Coming for Gas Power Generation

Last week the Wall Street Journal reported that,

“The [U.S.]industry installed 9.7 gigawatt-hours of new capacity between January and March, 32% more than in the year-earlier period and the most on record for a first quarter.”

Batteries (aka storage) are a gas demand assassin. Where batteries are showing up in the world they are destroying gas power generation demand.

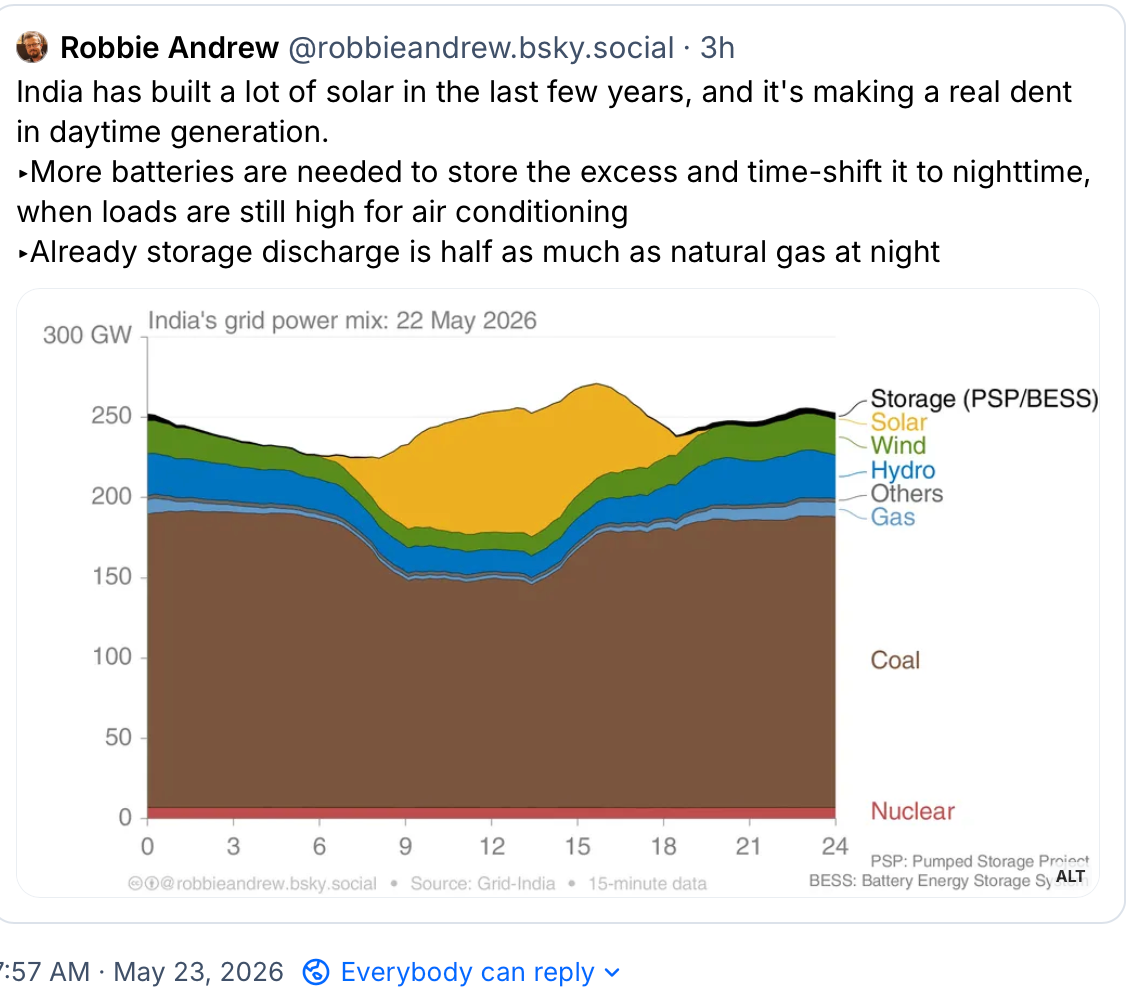

Robbie Andrew compiles data on India’s energy systems. India has just begun to build out storage to go with its rapidly growing solar assets. Already storage is supplying half as much electricity as natural gas at night in India. It’s also worth noting what is displacing coal use in India’s system and it ain’t gas.

Natural Gas Intelligence is starting to acknowledge this reality as well and included this in an article last week.

“Another year of strong solar growth could offset part of the demand increase from LNG exports, data centers and cooling load while allowing more gas to move into storage.

"It's part of the reason we've been able to keep prices in check in spite of rampant demand growth," Gonzales said.

Strong solar plus battery growth is the real key to explaining the low natural gas prices in the U.S. So what is happening in the U.S. power generation markets in 2026 in the U.S.?

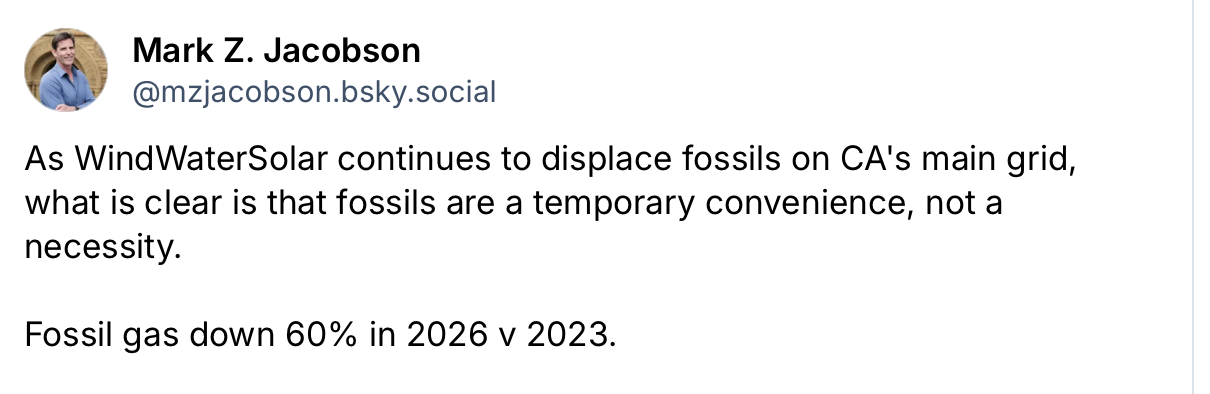

More of the same as the economics of solar plus storage are clear winners at this point. California is rapidly replacing gas demand with solar and storage. Mark Jacobson keeps us updated on the progress there. This is not a typo.

60% in three years! Guess what that does to California natural gas prices?

That was in April. Which led to this heading in an article in Reuters.

“TOO MUCH POWER IN CALIFORNIA”

A bit different from all of the headlines you read about how we don’t have enough power (for the oligarch’s data centers). Natural gas prices went negative in California in April. Very interesting framing to say that they have “too much power.”

Warmer Weather Working Against U.S. Gas Demand

While extreme weather is driving gas demand in some areas of the world, the increasingly warm weather is working against the gas industry in the U.S. Warmer winters mean less gas burn for heating. However, cooling demand peaks correlate with solar power peaks so the industry is losing winter demand and summer demand (see EIA chart above for the story of summertime gas demand in U.S. power generation). Winter demand losses are certainly due in part to all of the carbon dioxide and methane emissions created by the U.S. oil and gas industry. Since they are heating the whole atmosphere, U.S. consumers need less of their gas for heat. And heat pumps will be taking over more of that work anyway.

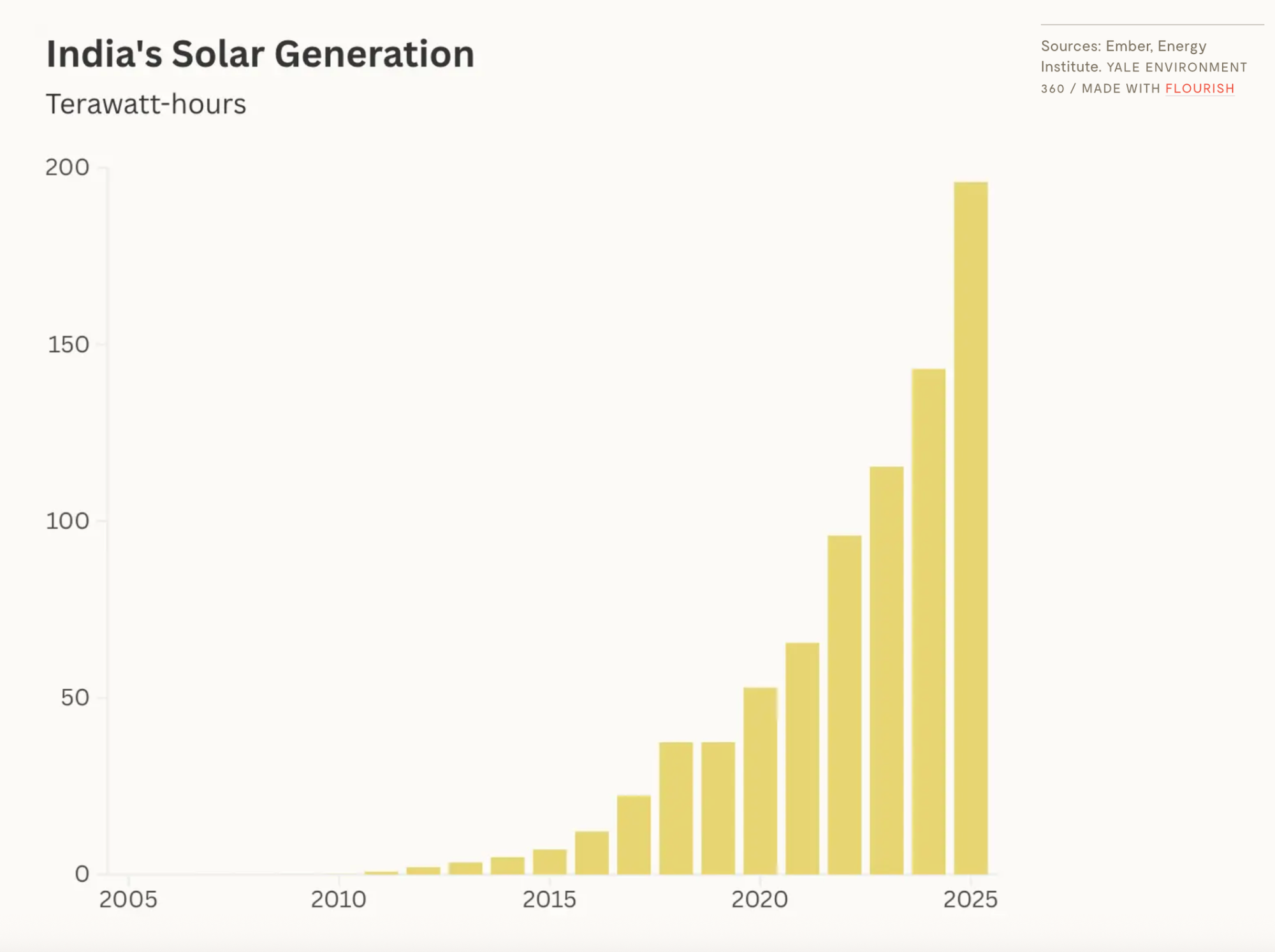

Meanwhile India is right now managing record power demand due to extreme heat. Why? Solar power. Last month Ember released a report saying India can produce 90% of its power needs with solar and storage.

Source: YaleEnvironment360

This article from last week on the rise of solar is worth a read.

“The question is no longer whether solar can power India’s electricity system, but how quickly it can scale.”

Remember we’ve been told that India is the country that will drive global LNG demand growth along with China. I’ve explained why this is highly unlikely and it’s a simple argument: solar plus storage is much much cheaper. In the game of power generation, low-cost wins.

It appears that fossil-fuel driven climate change is actively adding to natural gas demand destruction by warming up times of low solar (winter) which requires less natural gas for heating and gas not being able to compete with solar in the warm seasons.

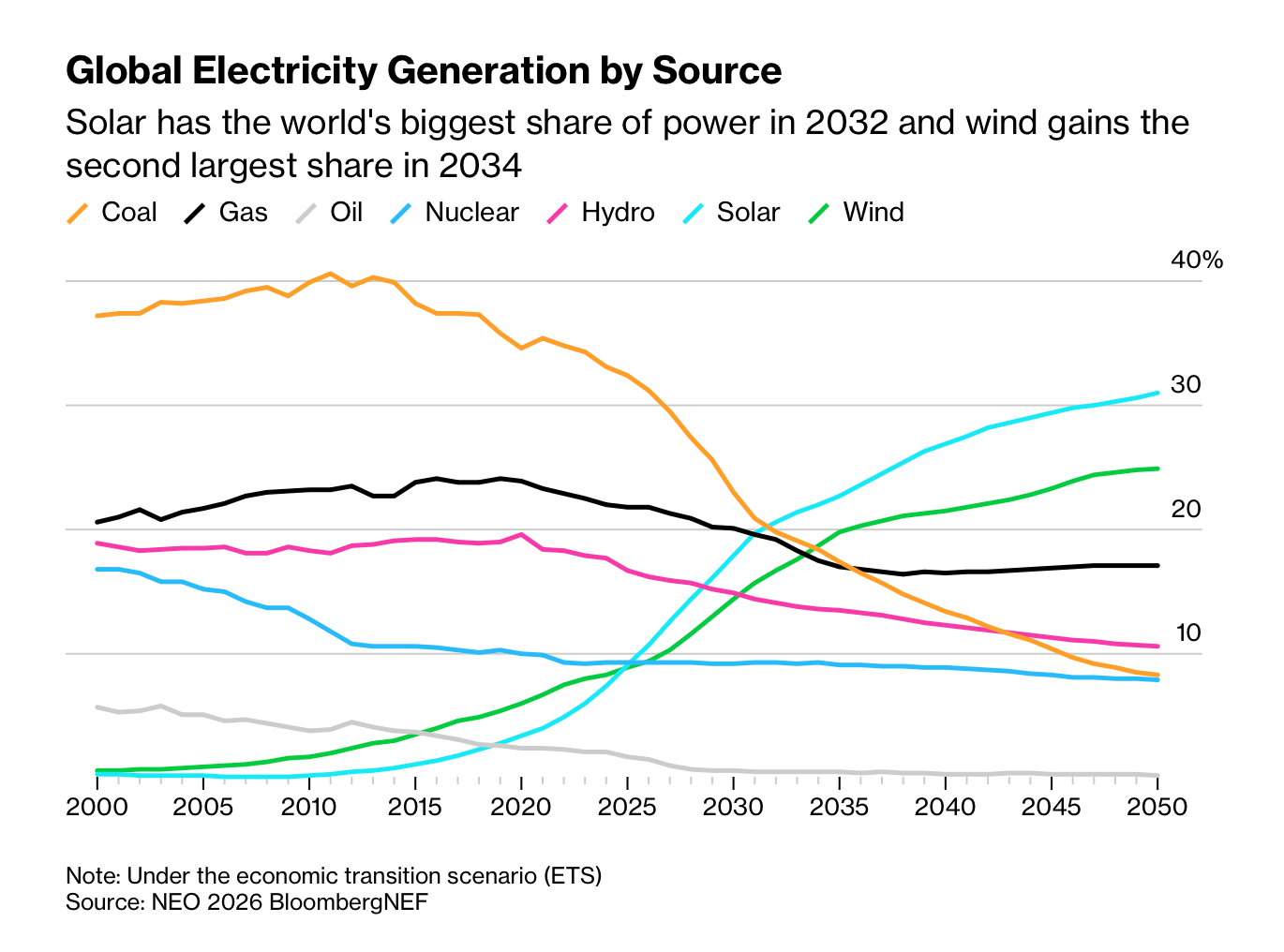

BNEF put out this chart recently. The black line is global gas. More expectations of demand destruction.

The oil and gas industry lectured us for decades that we could not switch to renewables because we couldn’t afford it. We were told that if latte-sipping liberals wanted to pay extra to make themselves feel better, they could, but the rest of the world would choose lower-cost fossil fuels. And they were right. But the tables have turned and now the low-cost solutions are not fossil fuels. When that happens, fossil fuel demand destruction follows. Expect more.

Update: I somehow wrote this piece and forgot to include this article that was published on Oilprice.com last week.

"Today’s massive gas plant buildout could eventually create stranded assets as renewables continue gaining market share and becoming the lowest-cost power source."

The article argues that natural gas could become "obsolete" in the future.

Comments ()