New Legal Complaint Questions Pioneer’s Sale to Exxon

A new legal action on behalf of a pension fund invested in Pioneer Resources is challenging Exxon’s purchase of Pioneer Resources with accusations that Pioneer CEO Scott Sheffield made a deal that was great for him personally — but not for shareholders. In February, the Operating Engineers Construction Industry and Miscellaneous Pension Fund, an investor in Pioneer Resources, filed a verified complaint for relief in Delaware requesting to inspect Pioneer’s books and records in regards to its agreed upon sale to Exxon. At the heart of the complaint are allegations “concerning potential breaches of fiduciary duty by members of the Company’s senior management.”

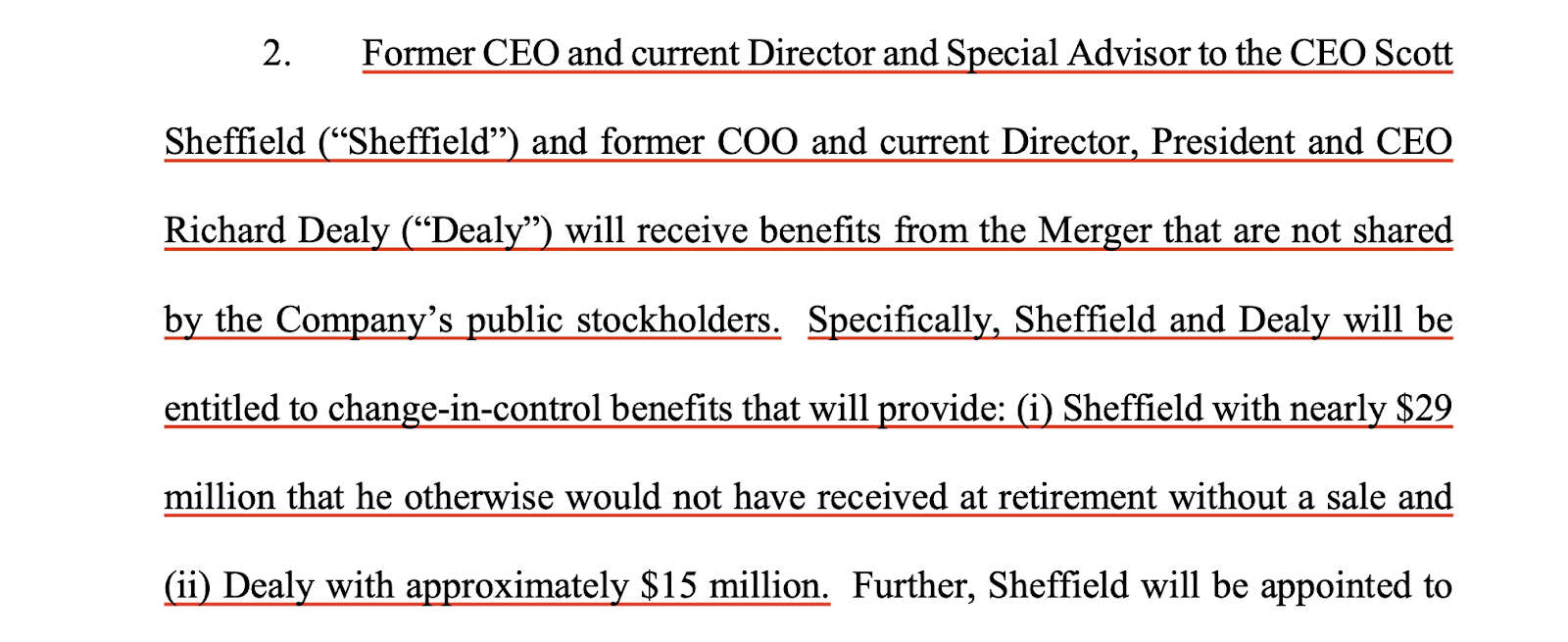

There are two interesting points about this complaint. The first is the argument that former Pioneer Resources CEO Scott Sheffield made a deal with Exxon CEO Darren Woods that was very good for Sheffield (and current CEO Richard Dealy) but not good for Pioneer Resources shareholders.

Source: Verified complaint for relief to compel inspection of books and records

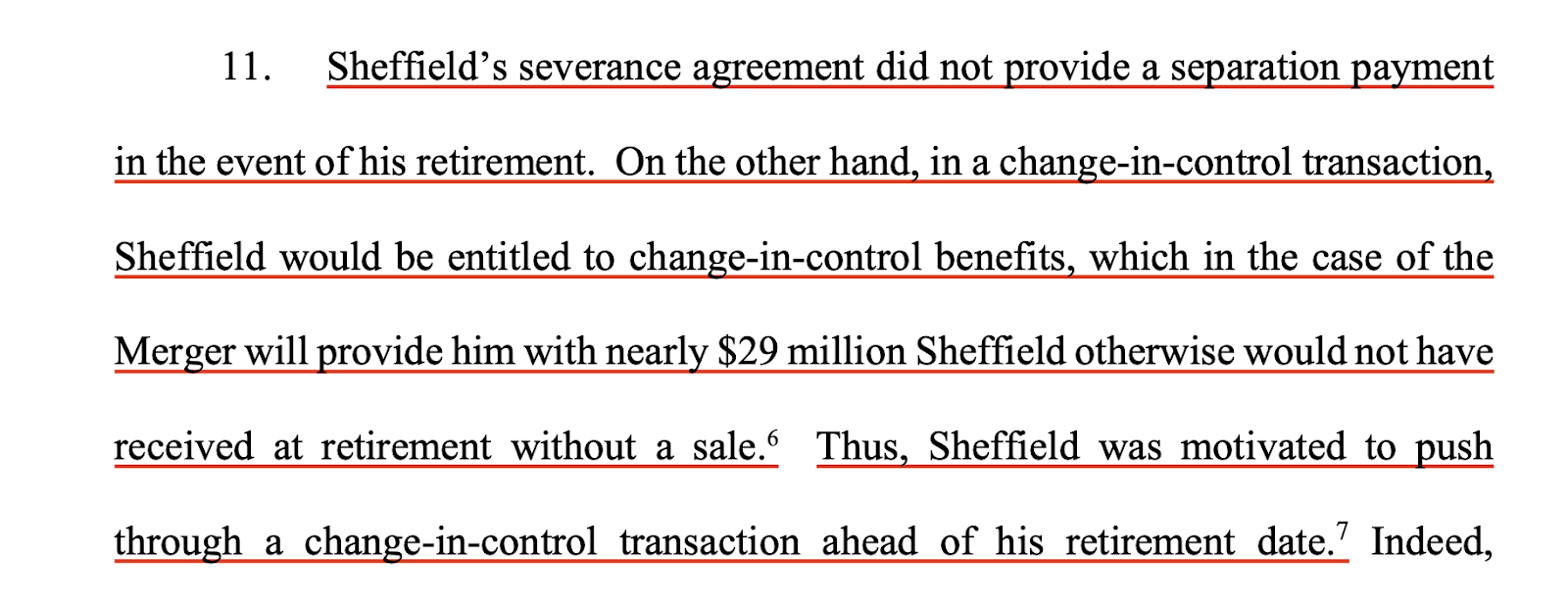

The main argument of the complaint is that Sheffield had strong personal incentive to make this deal happen before his planned retirement at the end of 2023. Specifically, the complaint notes that Sheffield had a “change in control” agreement that paid him $29 million extra if Pioneer was sold before he retired. Sheffield is also expected to get a seat on the board of Exxon as part of the sale, another valuable perk. These are the “benefits from the Merger that are not shared by the Company’s public stockholders” that are the basis for this complaint.

Source: Verified complaint for relief to compel inspection of books and records

Last month I wrote about how Sheffield changed his tune about the future prospects of the Permian once the Exxon deal was announced. The prospects for the $29 million bonus plus a seat on the Exxon board certainly could be one source of Sheffield’s newfound optimism about Permian oil production.

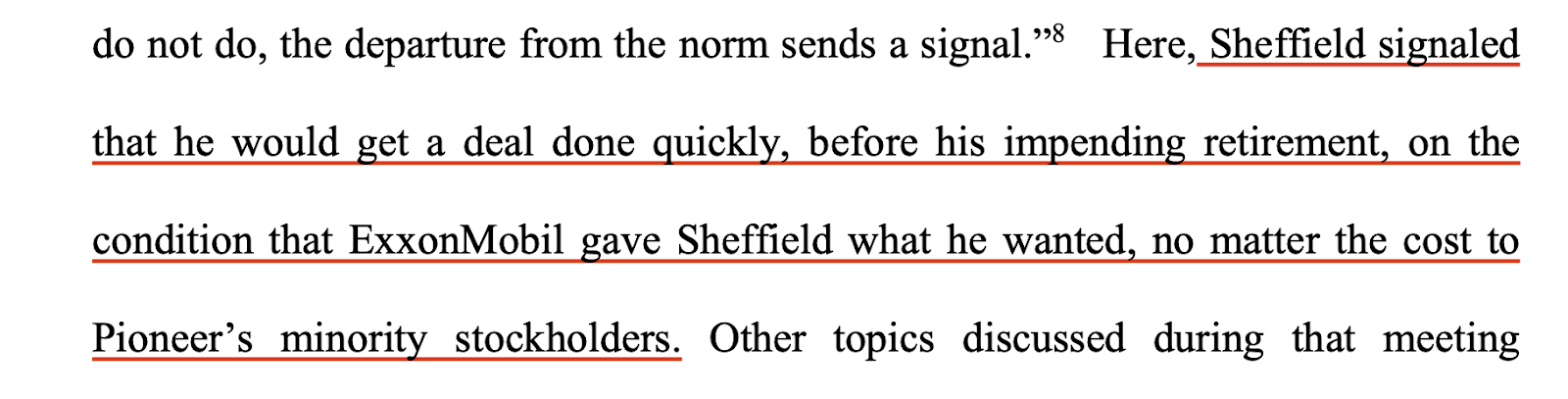

The complaint also alleges that Sheffield didn’t shop around for other potential buyers for Pioneer Resources, which if true, certainly seems like a suspect move by an executive looking to sell the company for its highest fair market value. The complaint says, “The Proxy provides that other than ExxonMobil, no other potential acquirors for Pioneer were contacted or solicited in the sale process.” The complaint appears to make the case that if Sheffield wanted his $29 million bonus, he only had one buyer that could meet his end of 2023 timeline.

Source: Verified complaint for relief to compel inspection of books and records

The complaint makes a compelling case that there are serious questions about this sales process. It’s worth a read for the full story including an odd detail where Goldman Sachs noted it had a conflict of interest regarding “its relationship with ExxonMobil,” but still played a role in the deal.

Alleged Hidden Environmental Liabilities

The second main argument in the complaint alleges that Sheffield and Woods hid environmental liabilities from Pioneer’s shareholders. This is quite interesting, especially since a lawsuit was just filed in Colorado by Client Earth on behalf of landowners that accuses oil companies of “fraudulent transfers” of environmental liabilities. The oil industry is eager to keep its true environmental liabilities off its books because, as this complaint makes clear, when the true liabilities hit the books, the stocks understandably lose value. The complaint also notes it has “credible basis” that Exxon was directly involved in the issue.

Source: Verified complaint for relief to compel inspection of books and records

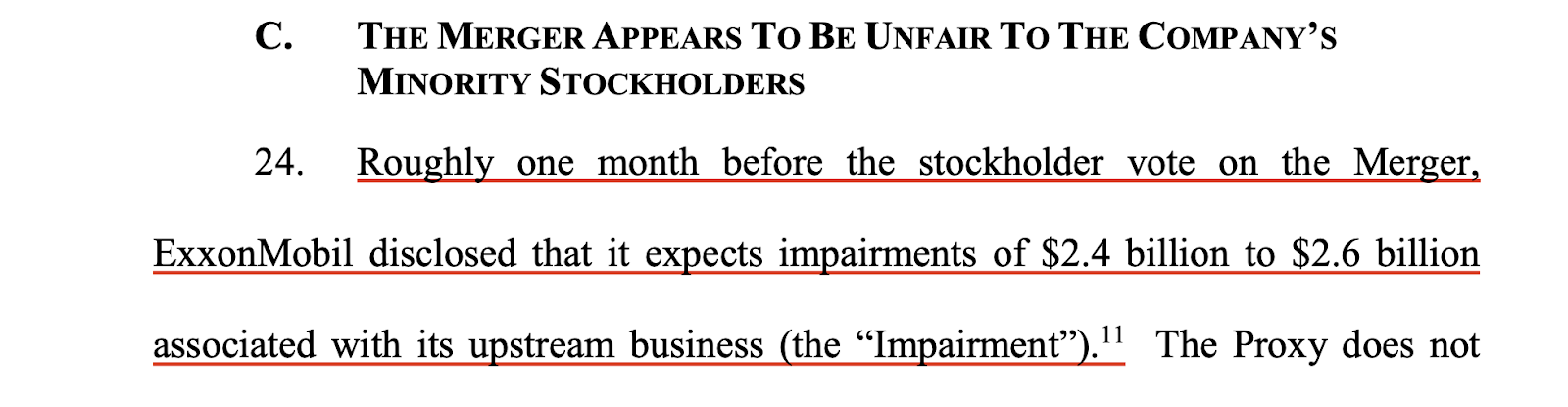

The true amount of environmental liabilities facing the U.S. oil industry is certainly being hidden from investors although, as the Client Earth case in Colorado shows, there are now efforts to make the industry actually pay to clean up its mess. And in the case of this complaint against Pioneer about Exxon's impairment, the number isn’t even that big — roughly $2.5 billion. While certainly a large amount of money, it is a fraction of the $20 billion writedown Exxon made in 2020 (that writedown was not for environmental liabilities but to reflect a more accurate value for its assets).

Source: Verified complaint for relief to compel inspection of books and records

In its disclosure to the Securities and Exchange Commission about the issue, Exxon stated that, “Impairments primarily reflect idle Upstream Santa Ynez Unit assets and associated facilities in California.” One asset. $2.5 billion. Exxon has a lot of such assets. Pioneer Resources shareholders likely aren’t going to like it when they learn about the size of potential future impairments for those assets. The complaint goes on to say, “After taking about a day to digest the news, ExxonMobil’s stock price declined significantly – over 5.5% – evaporating over $20 billion from ExxonMobil’s market capitalization.” It’s interesting to think about how much of Exxon’s market capitalization would evaporate if it was required to acknowledge all of its impairments.

The Times They Are A-changin’

While this complaint highlights issues that plague the industry like CEOs profiting while investors lose money and oil companies using bankruptcy to walk away from environmental liabilities, it also highlights an issue that would have been unimaginable in the past.

An oil company was acquired at a premium by Exxon. And at least some of the shareholders of that company are unhappy. Mostly because they are being paid in Exxon stock, not cash. These are people invested in the oil industry who apparently don’t want to own Exxon stock.

As I’ve been writing about the Exxon Pioneer deal and what it means for the U.S. shale industry, I’ve argued that the evidence is growing that if the American public wants the oil industry to pay to clean up its mess, it better get that money now, before the profitable oil runs out and the impairment bills come due. And like these Pioneer investors, it’s probably best to get that in cash instead of Exxon stock.

Comments ()