Is the U.S. Fracking Boom Based on Fraud?

In a 2016 interview with Fraud Magazine, former Enron CFO Andrew Fastow explained what he thought made him so successful while at the former energy corporation that’s now infamous for financial scandal.

“I think my ability to do structured financing, to finance things off-balance sheet and to find ways to manipulate financial statements — there’s no nice way to say it. Like I said at the conference, I was good at finding loopholes.”

As Fastow explained, in finance, the difference between a loophole and fraud isn’t always easy to identify. And that may be something the U.S. fracking industry is working to its advantage.

Fastow, the convicted fraudster, does admit that what they did at Enron misled investors. “We created something that was monstrously misleading, but any one of those deals alone wasn’t necessarily considered fraudulent,” he said.

Fast-forward to today and a different part of the energy industry: The U.S. shale oil and gas industry has lost more than a quarter trillion dollars since 2007, while being sold to investors as an economic boom, even at oil prices much lower than those of recent years. Does that financial mismatch seem misleading? Or perhaps, familiar?

In an unexpected twist, Fastow now gives talks to the energy industry on ethical leadership.

Sounding the Alarm

Bethany McLean was the first reporter to question whether Enron was a financially sound company in a 2001 article for Fortune magazine. McLean went on to co-author the book The Smartest Guys in the Room, which documented the fall of Enron due to its fraudulent practices, including the ones Fastow engineered.

In 2018, McLean also published the book Saudi America, which highlighted many of the financial challenges the fracking industry has faced. In a recent interview for Texas Monthly’s podcast Boomtown, McLean explained one of the very accepted and blatantly misleading practices of the fracking industry:

“I’d raise a couple of points. One is that companies have long hyped these break-even numbers. They say we can break even at $25 a barrel, we can break even at $20 a barrel. And then you look at their consolidated financial statements and they are losing money. And so something is going wrong … the people called it to me [sic] … corporate math or investor economics. So they were trying to put together these investor pitch decks that would show investors a set of economics that weren’t real. So they would show you that they could break even on a well at $25 barrel of oil but then yet you’d go to the corporate financial statements and they were losing money.”

Is that a loophole? Where you can openly misrepresent to investors the financial reality of your business? Or is it fraud?

As more and more players in the fracking industry run out of options and file for bankruptcy, investors are beginning to ask questions about why all the money is gone.

The Blank Check Companies

Much like with the housing crisis that caused the financial crisis of 2008, the fracking boom has led to Wall Street bankers finding innovative ways to finance a money-losing endeavor. Some companies are now even selling bonds based on future well performance, a concept similar to the mortgage-backed securities that led to the 2008 housing crisis.

Another Wall Street invention is what is called a “special purpose acquisition company” (SPAC), or, as they are also known, blank check companies. The way these investments work is a big bank or private equity firm backs a management team to raise money for the SPAC with the agreement that the leaders of the SPAC will then at some point make a “special purpose acquisition” — which means they will find an existing company and buy it.

They are called blank check companies because the management is given a blank check to buy whatever they choose. In the 1980s, the Wall Street Journal (WSJ) noted that “blank-check companies were often associated with penny-stock frauds.” In a 2017 article on the oil industry, the WSJ reported that “SPACs were a hallmark of the frothy days before the financial crisis [of 2008].”

Understandably, SPACs were often seen as a risky investment, but much like with the housing crisis, the biggest names on Wall Street are getting involved and giving the concept legitimacy, with Goldman Sachs starting to back SPACs in 2016. And new fracking companies have come about as a result.

Read the rest of the DeSmog series Finances of Fracking: Shale Industry Drills More Debt Than Profit

Ben Dell, a managing partner at investment firm Kimmeridge Energy, explained one of the risks of SPACinvestments to the Wall Street Journal. “SPAC management teams have an incentive to spend the money they have raised no matter what, so they can collect fees and pay themselves a salary and stock options at the company they purchase,” Dell said.

“SPACs are the most egregious example in the industry of executive misalignment with investors,” Dell told the WSJ.

As I have previously reported, one of the problems with the fracking industry is that CEOs are paid very well even when the companies lose money. According to Dell, SPACs take this problem to a new “egregious” level.

Alta Mesa: A Star Is Born

To successfully raise money for a blank check company, having some star power in the management helps. As the Wall Street Journal has noted, investments in SPACs “are largely bets on their executives.”

Jim Hackett would seem to be the ideal candidate to lead a SPAC in the fracking industry. Hackett has an impressive resume: the former CEO of fracking company Anadarko, former chairman of the Federal Reserve Bank of Dallas, an executive committee member of the industry lobbying group American Petroleum Institute, and partner at the major private equity firm Riverstone Holdings.

In 2013 Hackett retired from Anadarko to attend Harvard Divinity School to get a degree in theology. However, he was still a partner at Riverstone and in 2017 was lured back to the fracking business to run a SPAC backed by Riverstone.

The SPAC raised a billion dollars while being advised by the biggest names in the business, including Goldman Sachs and CitiGroup. The initial blank check company was called Silver Run Acquisition Corp. II.

Hackett used the money to buy two companies in Oklahoma — an oil producer and a pipeline — and the new combined company Alta Mesa was valued at $3.8 billion.

The Future Was Bright for Alta Mesa

Hackett and Alta Mesa had big plans for making money fracking wells in Oklahoma, which included forecasts for big increases in oil and gas production from the newly acquired assets with very low break-even numbers.

When the Wall Street Journal reported the creation of Alta Mesa, it noted, “Alta Mesa’s core acreage in Northeast Kingfisher County has among the lowest breakevens in the U.S. at around $25 per barrel, the company said.” Because oil was well over that price at the time, the future looked good, according to Hackett and Alta Mesa. Forbes reported that Hackett said Alta Mesa’s holdings were “oil that will be economic even at $40 WTI [West Texas Intermediate]” and oil has been well over that mark since Hackett made that statement in 2017.

Like break-even numbers, another area where misleading investors in the oil industry might be particularly easy is making overly optimistic forecasts about how much oil will be produced by future wells. The Wall Street Journal has documented this as a significant problem for the U.S. shale industry.

Description of Alta Mesa assets in investor proxy statement. Credit: Screen capture from proxy statement.

In early 2018 when touting the potential of the proposed new company Alta Mesa, Hackett said that “its average well would produce nearly 250,000 barrels of oil over its life.” A year later, Alta Mesa said it expected those wells would produce less than half that, only 120,000 barrels of oil over the life of the well.

In May last year, Alta Mesa was under investigation by the Securities and Exchange Commissions (SEC) “for possible issues in its financial reporting.”

Later in 2019, Alta Mesa filed for bankruptcy after writing down its assets by $3.1 billion. The billion-dollar blank check had been spent, and it took less than two years to lose it all.

SEC Investigation and Multiple Investor Lawsuits

Alta Mesa’s assets were sold off earlier this year. The SEC declined to comment on the status of the investigation.

In May 2019, the Houston Chronicle reported, “Alta Mesa also is facing a series of lawsuits. Some shareholders are suing claiming they were defrauded and lied to about the value of the company and its assets when the company was formed.”

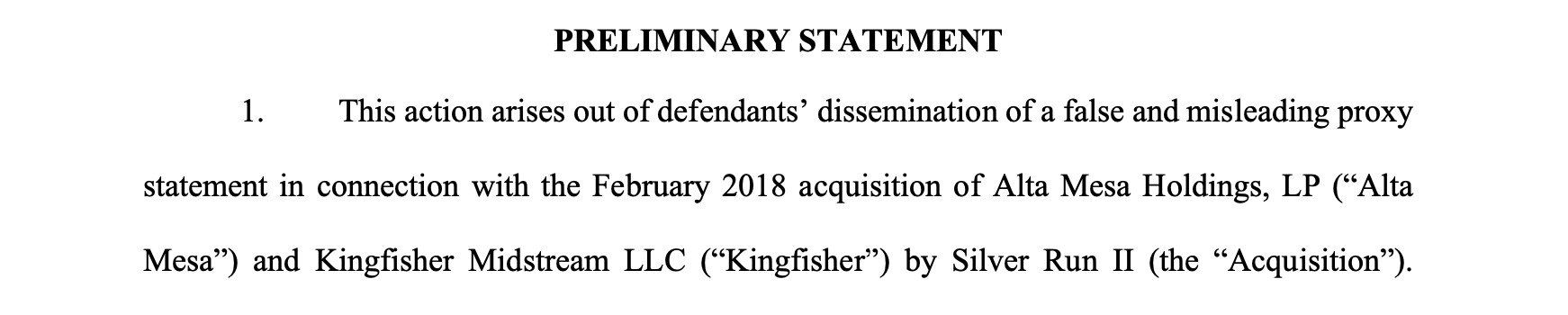

One lawsuit filed by the Plumbers and Pipefitters National Pension Fund claims that the proxy statement for Alta Mesa contained materially false and misleading information. That filing lays out a lot of facts to support that claim.

Statement for complaint for violation of the Securities Exchange Act of 1934. Credit: Screen capture of court documents

Another lawsuit alleges that Alta Mesa didn’t pay the proper amount of royalties to landowners, with state investigations into this issue.

Yet another lawsuit has been filed against Riverstone for “misleading statements.”

Investors are saying they were misled by Hackett and Riverstone. The allegations are based on the claims that were made about how much oil the company could produce. In hindsight, those claims appeared wildly inaccurate and misleading. But is that fraud? Or just taking advantage of a loophole?

In January, the Houston Chronicle summed up the situation as it described Alta Mesa’s downfall: “It was a dramatic fall from grace after significantly overestimating its potential in Oklahoma’s STACK shale play…”

While Alta Mesa is a spectacular example of how fast the fracking business can make large sums of money disappear after “significantly overestimating its potential,” it also likely marks the beginning of investor lawsuits against many other failing fracking companies with similar histories.

Learning From Enron

When Jim Hackett decided to go to Harvard Divinity School, several favorable profiles about his choice were written, including one on the Harvard website. That article noted that one of the reasons Hackett decided to go to school was because of “the collapse of Enron, a disaster that he attributed to ‘a failure in leadership’ among people he knew well.”

The speed with which Hackett and Alta Mesa went bankrupt is remarkable, indicating a likely failure in leadership.

However, Hackett seems to have learned something from former Enron executive Andrew Fastow: that there is work for former executives like them to teach the energy industry about ethics and morality.

Hackett is now a lecturer at the University of Texas at Austin Center for Leadership and Ethics.

Fraud? Or Just a Laughing Matter?

Good reporting is hard work but sometimes involves a bit of luck. Like when a Wall Street Journal reporter, in a room full of people hired to make forecasts of fracked oil and gas production, learned about the existence of much more accurate methods for predicting that oil production. And also learned that with accuracy comes much lower estimates of shale oil reserves.

The WSJ article that followed quoted Texas A&M professor and expert on calculating oil and gas reserves John Lee. “There are a number of practices that are almost inevitably going to lead to overestimates,” said Lee. Those are the practices used by the industry, with Alta Mesa serving as just one example.

Overestimates are why Alta Mesa received funding but now no longer exists.

The Wall Street Journal reported that during a presentation given by Lee, an audience member “stood up and challenged the engineers in attendance,” asking why the forecasters weren’t using accurate models like the ones that were available — as Lee had described.

Another audience member explained the reason.

“Because we own stock,” replied another engineer, “sparking laughter,” according to the Wall Street Journal.

Is it misleading to laugh at your company’s investors if you know the estimates you are giving them are inflated, but because you own the stock that benefits from those estimates, you do it anyway? Is that fraud? Perhaps that depends on if you get you get ethics lessons from Andrew Fastow and Jim Hackett.

Will the biggest innovation of the fracking revolution be making financial fraud a laughing matter?

A lot of people on EFT like to talk about how shale is fraudulent. That’s simply not true:

You can’t commit fraud when the rules are so lax you can just make shit up and it’s still allowed.

— Alpine High Fire Sale (@losingyourmoney) February 19, 2020

Read the rest of the DeSmog series Finances of Fracking: Shale Industry Drills More Debt Than Profit

Comments ()