Adventures in LNG Investing

LNG investors learning hard lessons about the major economic challenges facing US LNG exporters.

On January 22nd, in one of the many media articles promoting the recent initial public offering of U.S. LNG exporting company Venture Global, an investor commented on whether or not they thought it was a solid investment.

"We're torn on the deal, as the valuation looks high but it's a fascinating story," said a third investor

A week before that article, I was not torn on the deal as the numbers were pretty clear.

This is a classic pump and dump. They pissed off their biggest customers to make short term profits to cash out with an IPO.

Any idiots who invest in this deserve to lose everything.

Sadly it might be your pension fund manager.— Justin Mikulka (@justinmikulka.bsky.social) January 14, 2025 at 6:24 AM

Embedded JavaScript

However, I do agree with this anonymous investor that Venture Global makes for a fascinating story. So let’s take a look at the story as it seems these days investors don’t look at the numbers of a business or its future potential markets but instead prefer a good story (I think the kids call these memes).

The Beginning

In 2018 while writing about the movement of Bakken crude oil by rail I was researching the booming U.S. shale oil industry and started noticing a strange disconnect between what the oil and gas companies said about the finances of shale oil production vs. the actual financial numbers they reported. The main red flag was that they would say they could make money producing oil at a given number (say $45 a barrel) and then oil prices would be above that number for a quarter or the year and then the companies would report a loss. Turns out they were lying. When I began writing about this in 2018 I pointed out how the shale industry was just one more way for Wall Street to profit as they did in the housing bubble and I wrote, “...it is a spectacle. While the shale industry has lost over a quarter trillion dollars, it has been rewarded for this behavior.”

The U.S. shale industry was producing huge amounts of oil and gas and losing hundreds of billions of dollars in the process. And a lot of Wall Street bankers and shale oil CEOs got really rich while investors who believed them lost a lot. Remember this formula as we review Venture Global’s “fascinating story.” The U.S. shale boom was based on financial lies from the beginning and that worked great for Wall Street so why would they change? The Venture Global IPO and the current delusions about the future of the US LNG market may be the last act of the great shale oil and gas scam run by Wall Street (although there is always carbon capture!)

Angering Your Customers

Business school will make you cynical. You’ll learn things like “if you don’t offshore your manufacturing, your competition will” as a way to justify the “greed is good” approach to life and business. But even business schools avoid teaching a company to brazenly fuck over your biggest customers who are critical to your long-term business success. Sure you can poison them slowly or charge them illegal fees but don’t let them know you are doing it. And especially not if your business model is based on only having a handful of customers who sign 20-year contracts. But that is exactly what Venture Global appears to have done here.

Reading Venture Global’s Form S-1 Registration Statement (which they have to file before the IPO), it’s clear they understand that the basic business model of LNG exporters is dependent on securing long-term contracts. It’s also clear that their actions have angered all of their customers with long-term contracts. Here is my simple summary of what Venture Global did to their customers with their first functioning LNG export terminal.

Summary: Venture Global told their customers that there had been a “force majeure” event which, according to Venture Global, meant they did not have to honor their contracts with the major companies with the long-term commitments. And since spot prices of LNG were conveniently super high at the time, Venture Global instead sold a lot of LNG to people who weren’t their contract holders. How much? According to the S-1, “By September 30, 2024, we had loaded and sold 342 LNG commissioning cargos and received approximately $19.6 billion in gross proceeds from such commissioning cargos."

This was an excellent move for short-term financial gains for Venture Global, which they mention many many times in their S-1. How did their long-term customers respond to this? Venture Global did an excellent job of summing that up in their S-1, so I’ll quote them.

“All of such customers have questioned whether, and most have disputed in arbitration proceedings that, the delay constitutes a force majeure event, and they could assert that they are entitled to terminate their SPAs because COD did not occur by March 2024 … If we are unsuccessful in our current and any potential future arbitration proceedings with our customers, the amounts that we are required to pay may be substantial and certain of our post-COD SPAs may be terminated, which may lead to an acceleration of all our debt for the relevant project.”

Remember this was information that investors could have learned if they read the S-1. The S-1 makes it quite clear that if Venture Global loses customers for its first export facility it likely won’t be able to repay its debts, it likely won’t have money to finish its second project and the third-fifth fantasy projects will remain in the realm of fantasy. Did they read it? Or did they just read the articles saying Venture Global was going to be the biggest energy IPO in more than a decade and that it would be worth more than oil major BP? Is it reasonable to question why a company with one LNG export facility that has been plagued by operational issues would have a higher value than BP? It is but that would require you to ignore the “fantastic story!”

Knowing what we know about the business, you might think that Venture Global wouldn’t include a huge “fuck you” to two of those biggest customers right in their S-1 filing, right? You’d be very wrong about that!

BP and Shell are two of those big customers and the Financial Times deserves credit for pointing this out in their first article on the potential IPO when it was still being touted as $110 billion deal.

"Shell, BP and several other customers have filed arbitration claims worth $5bn against Venture Global, arguing it had reneged on long-term commitments to them to profit off the spot market."

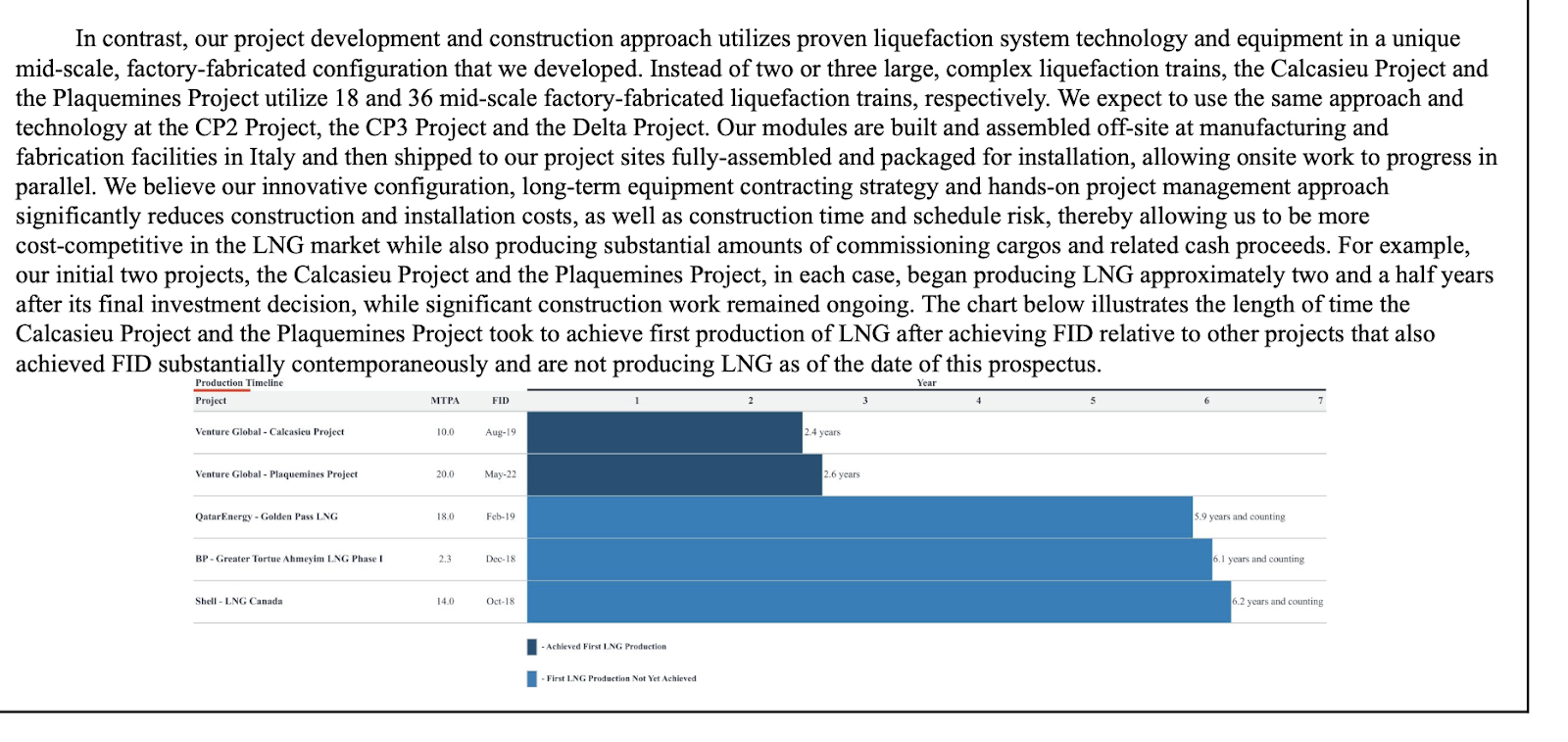

Remember that Venture Global told Shell and BP that they had equipment issues that caused the force majeure event that Venture Global argues gave them the right to not honor their contracts. In the S-1 they make the case that their equipment is superior to their competitors which allows them to get projects done much faster than other companies, which they illustrate with the graph below.

Source: Securities and Exchange Commission

You might notice both BP and Shell in this graph. So at the same time they weren’t honoring contracts with BP or Shell because they say their equipment isn’t working they were saying their equipment is far superior to BP and Shell and is “proven.” Who thought that was a good idea? I bet it wasn’t the person working on the arbitration cases. Do you think BP and Shell are inclined to work with Venture Global at this point? How about other major oil and gas companies? It’s not looking good. There are a lot of companies out there begging for long-term LNG contracts just like Venture Global and I expect BP and Shell are shopping around for more reliable suppliers. And the rest of the industry has clearly taken note.

“I don't want to deal with these guys [Venture Global], because of what they are doing. ... I don't want to be in the middle of a dispute with my friends, with Shell and BP,” Total CEO Patrick Pouyanne told Reuters.

That bit now has investors in Venture Global worried. Perhaps if they read the S-1 they would have seen this line. “Our ability to generate cash under our post-COD SPAs is substantially dependent upon the performance by a limited number of our customers, and we could be materially and adversely affected if certain of these customers fail to perform their contractual obligations for any reason.”

Venture Global told us that once they stop their “force majeure” operation and move into their normal business operation (post-COD SPAs) their business will be dependent on a limited number of customers (e.g. BP, Shell) and if those customers are unhappy it could impact their ability to “generate cash.” Want to guess how that is going to go?

The Big Flaw in the Venture Global Business Model

There is plenty to be concerned about with the Venture Global business model and the competence of management after they have scared off their customer base. I would argue that the biggest flaw (of many) is that the issue that has angered their largest customers and put this whole business at risk is not described as a one-time force majeure event that will not happen again but, I kid you not, as their unique business proposition.

“A key element of our business strategy is to generate proceeds from the sale of LNG at each of our projects during the commissioning phases of our projects, prior to the relevant project achieving COD.”

However, they do warn investors that they may not be able to pull off the stunt in the future.

“Historical proceeds from such sales at the Calcasieu Project, which has had an extended commissioning period due to unanticipated challenges with equipment reliability that we are in the process of remediating, may not be indicative of the duration of the commissioning period or the amount of proceeds for any future period or for any of our other projects.”

Can you understand why they wanted to do this IPO before the arbitration issues are settled? Are you wondering what sort of firm would risk their reputation to represent such a project in an IPO? Recognize any of these names?

How It’s Going

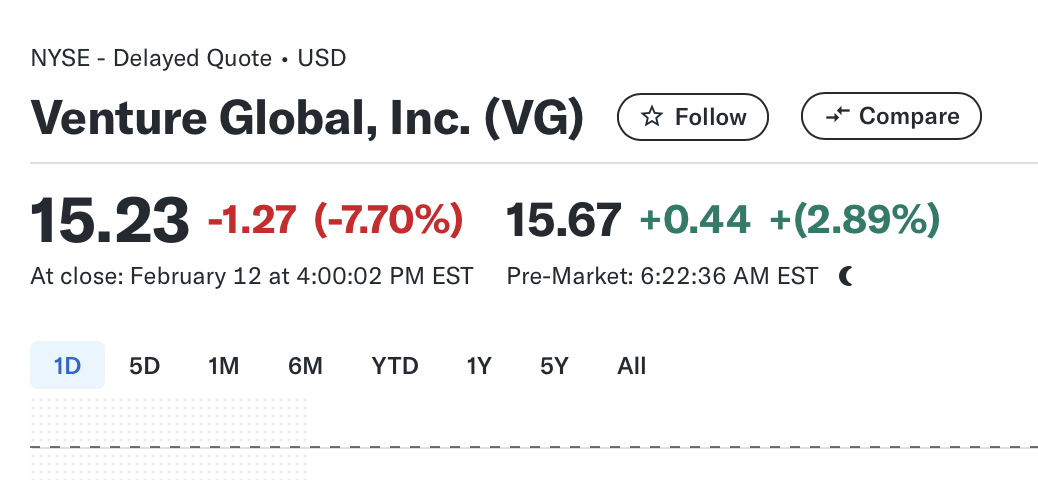

Initially Goldman Sachs and the other good people of Wall Street tried to sucker investors into paying between $40-$46 a share for Venture Global. That was a bit too fantastic of a story so they ended up doing the IPO at $25 a share. It is currently at $15 and change.

It’s now a third of the value that Goldman Sachs said it was worth when they were initially trying to sucker investors. The company that a month ago we were assured was worth $110 billion is now worth $36 billion (on paper). Remember, everyone lies about everything in the oil and gas industry. In hindsight, that is looking like a $70 billion lie right now.

I assume you can’t lie in arbitration hearings so perhaps that will be the beginning of people understanding the real value of Venture Global.

You may be wondering why the executives in charge of this company still have jobs as they appear to have built a company to fail. Don’t spend much time wondering. At the time of the IPO they were both worth more than $20 billion on paper. This is the real fascinating story of the shale boom. It has all been a pump and dump scheme. Investors lose money while executives acquire fabulous wealth with the help of their friends on Wall Street.

Comments ()